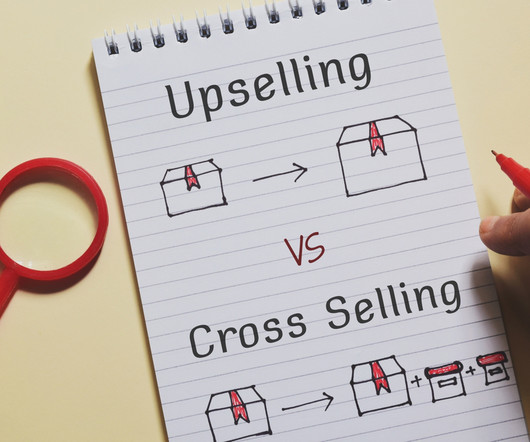

Cross-Selling and Upselling – 2 Drivers of Relationship Profitability

South State Correspondent

MARCH 19, 2024

In two previous articles ( here and here ) we discussed how loan size and loan term affect the profitability of commercial loans. We continue this theme of major drivers of loan and bank profitability and discuss the importance of cross-selling and upselling, and its impact on bank performance. In this article, we consider the common features of upselling and cross-selling.

Let's personalize your content