Overcoming Lending Challenges for Community Banks

South State Correspondent

JULY 5, 2020

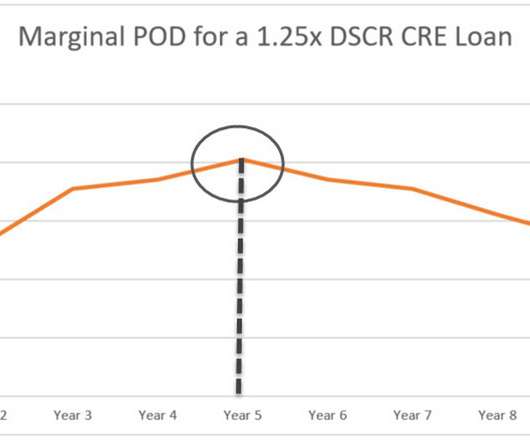

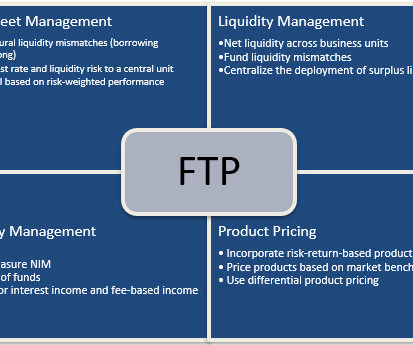

Covid-19 and the responses to the pandemic are exerting various pressures on community banks. How a community bank underwrites and books commercial credit through the end of 2020 will have a significant impact on the bank’s profits and credit quality through the entire next business cycle.

Let's personalize your content