2022 Dodd-Frank Stress Test Scenarios Released

Perficient

MARCH 3, 2022

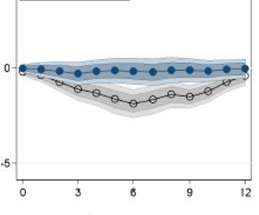

The Office of the Comptroller of the Currency (OCC) recently released the economic and financial market scenarios that will be used in the upcoming stress tests for covered institutions. As repeated by federal bank regulators, the required economic scenarios are not forecasts. The 3-month Treasury rate increases from 0 percent to 1.5%

Let's personalize your content