Loan Hedging for Community Banks in 2024

South State Correspondent

JANUARY 10, 2024

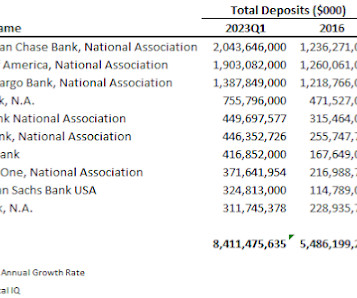

Community banks’ use of swaps (banks’ primary tool to hedge interest rate risk on loans) has increased substantially over the last ten years. Meanwhile, community banks face net interest margin (NIM) and fee income pressure. Only 304 banks (or 6.7% of the total) used swaps directly.

Let's personalize your content