What #Banking Trend Will Have the Greatest Impact on Your Bank?

Jeff For Banks

APRIL 4, 2024

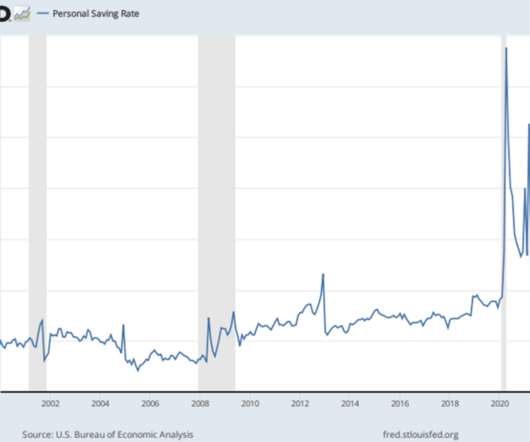

And then what happened in 2004-06 happened again. The Fed has paused for nearly a year now, and it was our experience in 2006-07 that bank cost of funds continued to increase as the market closed the delta between what someone could earn in a money market mutual fund and a bank account. Cost of funds is leveling off now.

Let's personalize your content