A year ago, solidifying a digital business was still at the level of a “nice to do” for most SMBs. A year and one global pandemic later, digital transformation has become a need-to-do for SMBs looking to survive the storm. Luckily, PYMNTS can offer some guidance in the form of four concepts every SMB should investigate as they look to build out digital expansion.

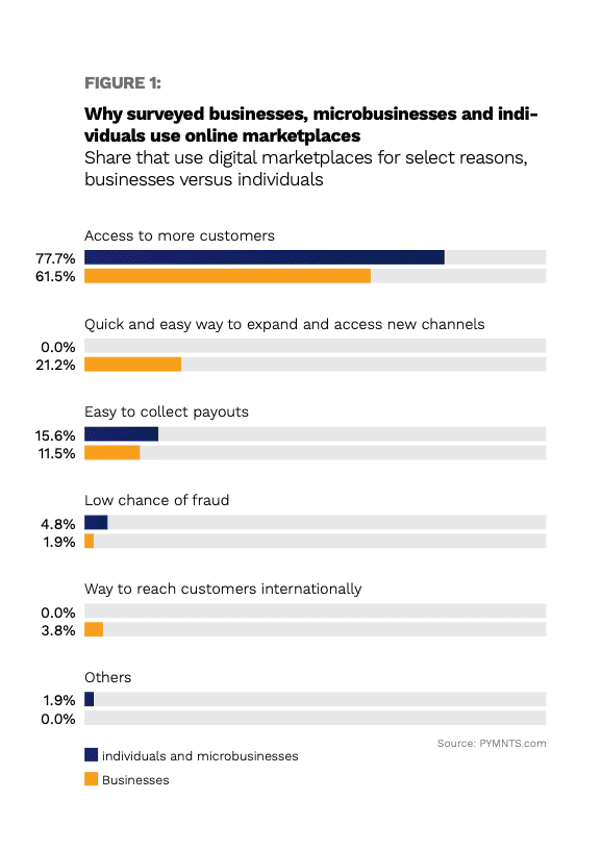

When merchants were surveyed by Visa, two very interesting facts emerged. The first is that 60 percent of retailers have a problem: They aren’t currently selling on marketplaces, despite the fact they would like to do so. Among the 40 percent that are selling on marketplaces, 60 percent noted that they would be willing to take their business to a new marketplace that offers real-time settlement.

Mike West, head of global commercialization for Visa Direct, told Karen Webster that cash flow is the “life’s blood of any business” – and yet when it comes to marketplace payments, merchants’ leading concern is that they are often left waiting days, and sometimes even weeks, for payments on their sites to settle. Without those funds in hand, he noted, those businesses can’t pay bills, re-up their inventory or pay their workers, which means slow settlement is a true pain point.

Real-time settlements — where funds are transferred quickly between banks, such as those facilitated by Visa Direct — can help close those cash-flow gaps as these smaller firms navigate the day-to-day challenges of buying inventory, paying bills and covering shipping costs. Forward-thinking marketplaces are quickly realizing this is the offering they need to make now.

“We’re seeing really strong adoption from a lot of marketplaces now” that are realizing the value of real-time settlement, said West. Selling on a marketplace, he noted, is “going to be a new normal.” The ones that win will be those that realize SMBs will naturally gravitate to those that pay instantly.

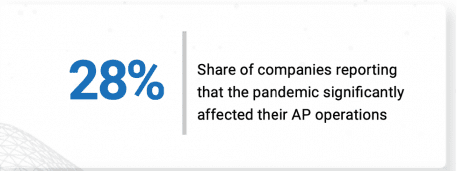

As businesses have been digitizing their front-end experiences to meet consumers’ shifting needs, there has been a growing need to bring the backend up-to-date and paper-free, as firms are realizing that paper-dominated, manual processes are too slow to function in the digital era.

Legacy accounts payable (AP) processes often drain businesses’ budgets, cost employees time and create opportunities for human error. Sixty-five percent of SMBs said a key B2B payment friction stemmed from the fact that “manual payment generation workflows are error-prone and time-consuming.” As the data demonstrates, automation can pull data from received invoices, match the details against purchase orders to check for errors, and route the invoice information through company systems for payment approvals – thus drastically cutting back on both manpower used and mistakes made.

Those without systems to detect such errors may pay twice – and these mistakes can cost SMBs more than $12,000 per month on average. AP modernizations can help prevent this, potentially cutting costs by 30 percent to 50 percent. Greater efficiency also allows SMBs to negotiate better payment terms for themselves and effectively determine what payment arrangements work to their advantage, the data shows.

The economic fallout resulting from the pandemic has further pressured SMBs to closely examine their cash flows and ensure they are leveraging any and all savings opportunities. Relying on AP automation tools could ultimately help SMBs build more resilient, efficient operations.

In many cases, this year has meant that SMBs needed more than an efficiency upgrade – they also needed access to additional funds. And yet when they sought out those funds, they found that mainstream banks were often lacking when it came to offerings.

“As an entrepreneur, I understand the frustrations many businesses face when dealing with their banks,”said Lee Bushell, chairman of the Bushell Investment Group, of the rollout of Birmingham Bank to help U.K. businesses. “As we roll out the Birmingham Bank, we aim to simplify banking and focus on the underlying relationship between ourselves and our customers. In an age of FinTechs and large banks, we will sit squarely in the center and use technology to make banking needs simpler — but use experienced people to make common sense-based decisions.”

The move, according to Andy Street, mayor of the West Midlands, where the new bank will operate, says the addition will be a great boost for the region’s economy and will play an important role in supporting local businesses. “Small- and medium-sized businesses are critical to our economy and jobs, and having this new bank embedded in the region will help provide them with the financial support that is more crucial now than ever,” Street said, according to the report.

SMBs that managed to hold on through the pandemic are now ready to move onto the next phase. As Visa’s Global Head of Business Solutions Kevin Phalen told Karen Webster in a recent discussion, they are now ready to go on to the next phase in 2021, using those same tools to thrive in the emerging digital ecosystem.

SMBs that managed to hold on through the pandemic are now ready to move onto the next phase. As Visa’s Global Head of Business Solutions Kevin Phalen told Karen Webster in a recent discussion, they are now ready to go on to the next phase in 2021, using those same tools to thrive in the emerging digital ecosystem.

“The good thing is, despite all of those negatively impacted to the point of failure, the businesses that have embraced digitization and new technology are actually more optimistic, because they believe their client base has expanded. They have found new clients through embracing this digital transformation,” Phalen said.

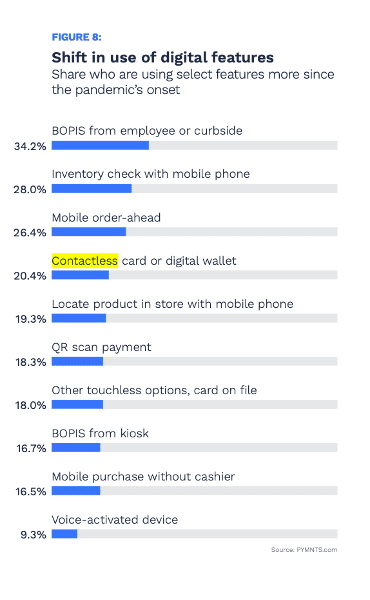

According to Visa’s data, 82 percent embraced new forms of digital technology to meet their consumers’ emerging need sets. Some 47 percent are integrating security and fraud management software, 44 percent are embracing contactless or mobile payments, 36 percent are integrating buy online pick up in-store (BOPIS) and 31 percent are upgrading digital backend payment operations.

And beyond that, Phalen and Webster agreed, they’ve opened up to adapt to a radically shifting market, with examples ranging from hairdressers shipping product kits out to homebound customers to restaurants offering meal kits and grocery services. SMBs now know, he said, that the time has come to pivot their thinking.

As for what those second-phase efforts will entail, Phalen noted that security will be a leading area of interest, particularly for SMBs that are experiencing their first run-ins with cybercriminals. Reinventing the backend to match the now digitized front end will be a leading concern, along with integrating technologies that make it easier for consumers to seamlessly and simply move across channels.

The Visa study is validated by PYMNTS research that shows consumers’ use of BOPIS and contactless payments.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More