COVID-19 has closed bank and credit union (CU) branches across the United States, sending the demand for digital banking solutions soaring as consumers hop online to manage their finances from home.

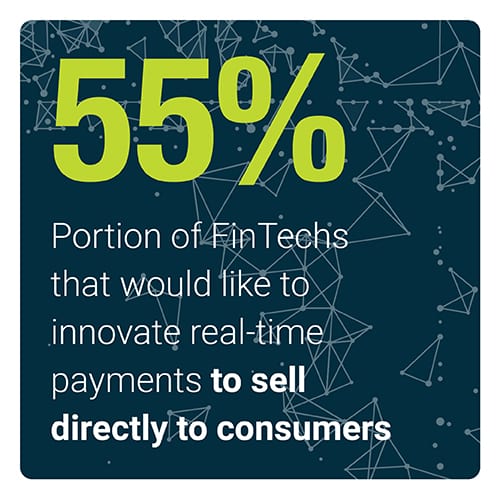

However, CUs are not the only financial institutions (FIs) looking to offer digital banking innovations to their members. FinTechs are also emerging as major CU competitors. Among FinTechs that are interested in developing new peer-to-peer (P2P) payment, real-time payment and installment credit products, PYMNTS research shows that half intend to sell those products directly to their end-users. This puts FinTechs and CUs on a collision course, with each racing to innovate new products that will grab members’ attention and patronage.

However, CUs are not the only financial institutions (FIs) looking to offer digital banking innovations to their members. FinTechs are also emerging as major CU competitors. Among FinTechs that are interested in developing new peer-to-peer (P2P) payment, real-time payment and installment credit products, PYMNTS research shows that half intend to sell those products directly to their end-users. This puts FinTechs and CUs on a collision course, with each racing to innovate new products that will grab members’ attention and patronage.

This so-called “FinTech challenge” is compounded by the fact that 45.9 percent of CU members would consider switching to technology firms, if they could provide the same services their CUs provide at a better price or with a better user experience.

So which innovations are CU members most interested in using? And how can CUs ensure that the  financial products they develop will meet their members’ expectations and keep them loyal?

financial products they develop will meet their members’ expectations and keep them loyal?

These are just a few of the questions PYMNTS sought to answer in the latest Credit Union Innovation Playbook: New Payment Flows edition, in collaboration with PSCU. We surveyed 4,058 U.S. consumers on the digital banking features they are most interested in using to find out which technologies will help drive innovation in the financial sector going forward. PYMNTS also surveyed 100 CU leaders about the innovations they are planning to develop and 50 FinTech executives about their interest in selling products directly to consumers to learn more about which innovations they are prioritizing — and which innovations consumers will actually use.

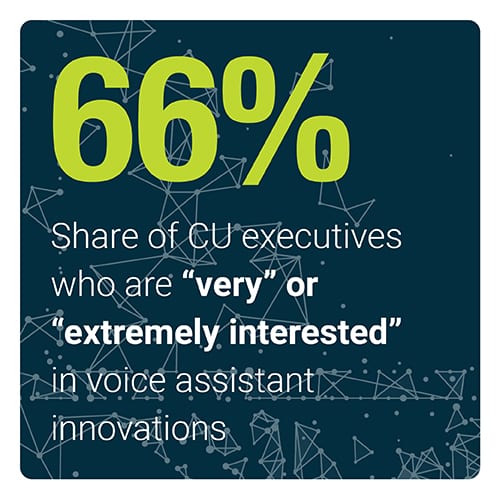

Our research shows that P2P payments and voice assistant features are among the digital products in which CU members are most interested, for example, with about one-third of all members citing interest in at least one of them. Credit unions appear to understand that these technologies are in high demand, with 66 percent interested in prioritizing voice assistant innovations and 55 percent interested in prioritizing P2P payment innovations. In this regard, CUs are well-positioned to meet their members’ demands for digital payments services.

Our research shows that P2P payments and voice assistant features are among the digital products in which CU members are most interested, for example, with about one-third of all members citing interest in at least one of them. Credit unions appear to understand that these technologies are in high demand, with 66 percent interested in prioritizing voice assistant innovations and 55 percent interested in prioritizing P2P payment innovations. In this regard, CUs are well-positioned to meet their members’ demands for digital payments services.

Just providing these services is one matter; making sure those services meet consumers’ expectations is another. Member satisfaction with their CUs hinges on their ability to deliver easy-to-use and convenient payment services in a timely manner, with 66.2 percent and 72.5 percent of consumers citing these factors as reasons for their satisfaction. Failing to deliver innovations that provide the user-friendly and timely services members expect could drive them to seek services at FinTechs, other CUs and even non-FI businesses, such as large retailers.

So, just how great is the competitive threat to CUs posed by such businesses? How likely is it that members will leave their CUs to bank with them, and what can CUs do to ensure their innovation plans meet their members’ expectations?

The answer to these questions and much more can be found in PYMNTS’ Credit Union Innovation Playbook: New Payment Flows edition.

To learn more about the digital banking solutions that are driving innovation in the financial sector, download the Playbook.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More