The arrival of 2021 brought fistfuls of studies, all highlighting exponential growth in the use of technology spurred by the pandemic. Among those was a study released by JPMorgan Chase, which featured new data showing just how many people are using digital features throughout the financial industry.

To continue the theme, the New York-based megabank pursued the topic further this year and found almost nine out of 10 people are depositing their money at their financial institution via mobile phone. The results came from a survey of over 2,000 between the ages of 18 and 57+. The survey occurred in late April and was published in August 2021, which Chase confirmed with The Financial Brand consisted of non-Chase consumers.

Read More: How Mobile Deposits Are Broken (And How to Fix Them) )

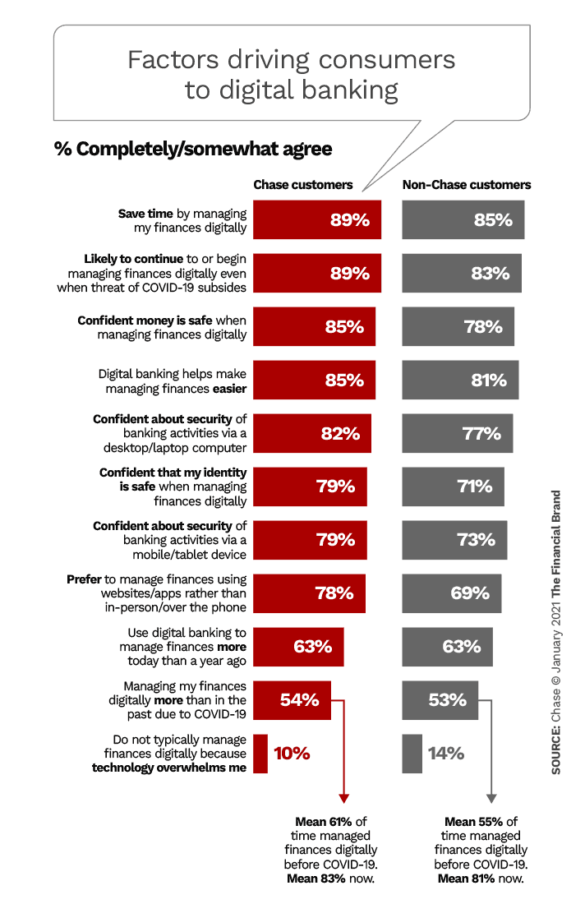

For good or for bad, the pandemic changed how much of the world banks. Back in January 2021, these factors were driving people to digital banking.

As Covid-19’s impact starts to level out in the U.S. — more of the country is getting vaccinated, seen as a hopeful sign, even as the Delta variant spreads — the digital banking tools people came to depend on during 2020 appear to be a permanent fixture in their banking habits. The Chase survey backs up the theory: Avid consumer interest in technology from financial institutions continues.

Food for Thought:

Nearly 90% of those surveyed by Chase say they’re depositing their money through their financial institution’s app. Is your financial institution’s mobile game keeping up with consumer demand?

Cash Is Still on the Critical List

Just as streaming replaced Redbox, which revolutionized the DVD, which had already replaced the VCR tape, payment services have quickly upgraded from cash to contactless cards on people’s cell phones.

Gill Haus, Head of Digital Technology at Chase says the company has noted that cash — while being used less frequently — is still “an important form of payment for many of our customers.”

However, even as the country gets vaccinated, it appears people still don’t want as much cash in their wallets they once did. 13% of both Baby Boomers and Gen Z say they “would not feel comfortable using cash again, even post pandemic,” according to the Chase report.

As a result, many industry experts are looking to contactless payments as the wave of the future. Almost half — 47% — of those consumers surveyed across the generations say they have started and/or continued to utilize these mobile options just to avoid physical interactions. Nearly three-fourths of respondents consider them a more convenient way to pay.

Read More: Mobile Banking Apps Failing in Key Areas of CX

Chase expects these contactless forms of payment to only increase in popularity, Haus says.

“Our customers have increasingly been using Zelle to send money or to split the cost of bills through our mobile app or on Chase.com,” Haus says. For context, he explains that Zelle’s network of hundreds of banks and credit unions “processed 1.2 billion transactions in 2020, totaling $307 billion sent — an increase of 58% and 62% respectively year-over-year.”

At the same time Chase released its survey, Bank of America announced that 85% of its deposits were made digitally in its 2021 fiscal second quarter. The bank boasted that, at the beginning of July, seven out of every ten Bank of America customers were using digital channels for more of their needs.

“We are delivering the best financial technology to help make our clients’ financial lives better,” says David Tyrie, Head of Digital at Bank of America. “To elevate each client’s digital journey across their entire relationship with us, we focus on their unique needs and aspirations so that we can deliver individualized digital experiences.”

The “branch or no branch” argument, going for years before Covid, has ramped up in the wake of the pandemic and worldwide shutdowns. Even when the U.S. banking industry thought it was witnessing the beginning of the end of the Covid-19 pandemic, consumers were still relying on their financial institutions’ mobile apps. As mentioned before (and in line with Bank of America’s news), Chase says nearly 90% of people are using a mobile app to deposit their money, with over half (52%) of Baby Boomers doing so.

Don’t Fall Prey:

Regardless of where the pandemic stands in the U.S., people aren’t going to stop expecting high-quality mobile banking apps.

Personalization Is Paramount

Unsurprisingly, people favor personalization. Who is going to argue that an individualized experience wouldn’t matter when interacting with their financial institution, either online or in-person? However, there are touchpoints in their banking journey where consumers want even more personalization.

For instance, Chase found that nearly every one in two people (48%) wish their banking providers would integrate more personalized banking data insights (such as saving and spending habits) into their customer strategies. And 79% of Gen Zers — which the banking industry is scrambling desperately to understand better — say they wish their bank or credit union would provide more personalized offers and information so they can save at their favorite retailers. (Compare that result to the 41% among all respondents).

Read More: Bank of America Grabbing 1 in 3 Gen Zs and Millennials with Mobile )

To keep up with this demand for more customization, many financial institutions are trying to fuse AI solutions with their digital banking systems. Yet it’s essential that banks and credit unions alike focus on not only the technology, but the customer experience as well. For instance, in a new study focused specifically on Georgia banking customers, Foresight Research suggests consumer adoption of AI technologies won’t be easy.

However, the report also notes that people who are already satisfied with their financial institution’s performance when it comes to problem solving and automated financial advice will be more likely to be comfortable with AI software. “The overall customer experience seems to be a prerequisite to automated banking adoption,” Foresight suggests.

At the end of the day, it will require banks and credit unions to utilize AI in their banking strategies to maximize the customer experience.

“Machine learning and artificial intelligence power many of our personalization efforts today,” Haus says. “For personalization to be useful, financial institutions have to present their customers with insights that are actionable and easy to digest.”

All About That Savings

Just as the financial crisis of 2008 instilled fear in consumers, 2020’s Covid-19 pandemic drove heightened consumer reliance on the savings account.

Chase said in its 2020 Digital Banking Attitudes Study that 40% of people said they “looked forward to contributing more to their savings accounts in 2021” as financial institutions also start to invest in more automation tools.

Automatic saving features could be a saving grace for people if concerns about the Delta variant’s influence in autumn 2021 are confirmed, especially if the United States endures a second wave of shutdowns. 84% of people say they’re using these automated tools for savings, and the trend is only likely to gain more traction.

Additionally, as more consumers shift to mobile banking apps as a primary channel, they’re able to check their balances daily and keep track of their spending habits. This new luxury is helping people save — over 40% of people say seeing their debit and credit card usage encourages them to better understand their cash flow.

Read More:How the Best in Banking Are Marketing Their Mobile Apps