Best practices for credit risk management in uncertain times

Abrigo

OCTOBER 14, 2022

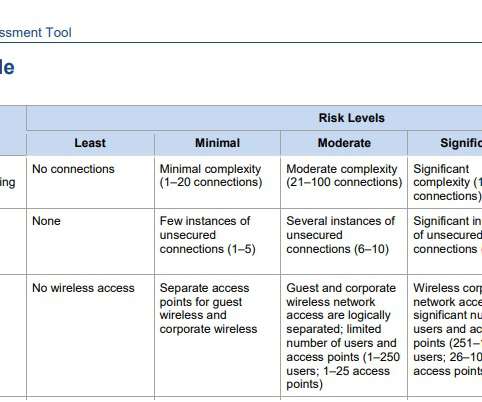

Fortify your credit risk management framework How to prepare your organization for scrutiny of its credit risk management practices during your next exam or review. . You might also like this whitepaper, "Stress Testing: Managing Capital Levels and Credit Risk."

Let's personalize your content