The report: Scaling to $1 Million: How Small Businesses Fare by Owner Race and Gender [April 2024]

Source: JPMorgan Chase & Co. Institute

Both economists and policymakers agree the small business sector is a significant contributor to the American economy. However, most small businesses are just that — small — and while they generate wealth for their owners, most have no employees and limited revenue. As a result, policymakers aim to help smaller businesses scale and grow, particularly those owned by people of underrepresented demographic groups.

JPMorgan Chase studied financial data from 835,000 small businesses and found notable disparities between the growth trajectories of small businesses led by white owners and those led by underrepresented demographic groups. By expanding lending options to these communities, banks and financial institutions may be able to reduce the gap.

Key Takeaways

- Black and Hispanic-owned firms are less likely than white and Asian-owned firms to reach $1 million in revenues within five years of starting a business. Female-owned firms were also less likely than male-owned firms to reach that milestone.

- The research found that half of those who reached the benchmark did so in the first year, suggesting the high performers had more access to startup capital.

- Products and policies that support personal wealth building to alleviate gender and race gaps may offer small business owners more personal financial capacity to support business development, which, in turn, could drive more economic growth.

- JPMorgan Chase suggests that policymakers in the public and private sectors could help address opportunities and barriers to growth. Meanwhile, banks can design growth capital solutions to target the needs of companies that are most likely to scale.

What we liked: The report authors conducted deep research to demonstrate how a lack of startup capital puts companies owned by underrepresented demographics at a disadvantage.

What we didn’t: Chase spent a lot of effort to lay out the problem, but its focus solely on the $1 million benchmark may have overlooked greater disparities in the general small business market. The report is also short on solutions, with little more than generic advice to improve product awareness and lending access.

Racial and Gender Disparities on the Path to $1 Million Revenues

Chase used business banking transaction-level administrative data and tracked small businesses from the beginning of their business banking activity through their first five years of business. The sample included an analysis of 835,000 small businesses between January 2011 and February 2020.

Year 1 to 5 revenues: The typical small business had annual revenues below $100,000 in its first years and only 9% reached the $1 million milestone at least once within five years. However, nearly half of those firms that reached the milestone did so in the first year.

“Banks and other financial institutions may not be optimally positioned to meet all small business financing needs. However, innovative efforts to expand services to business owners of color and female business owners could provide more growth-intentioned small businesses a stronger start in the first year of business and beyond.”

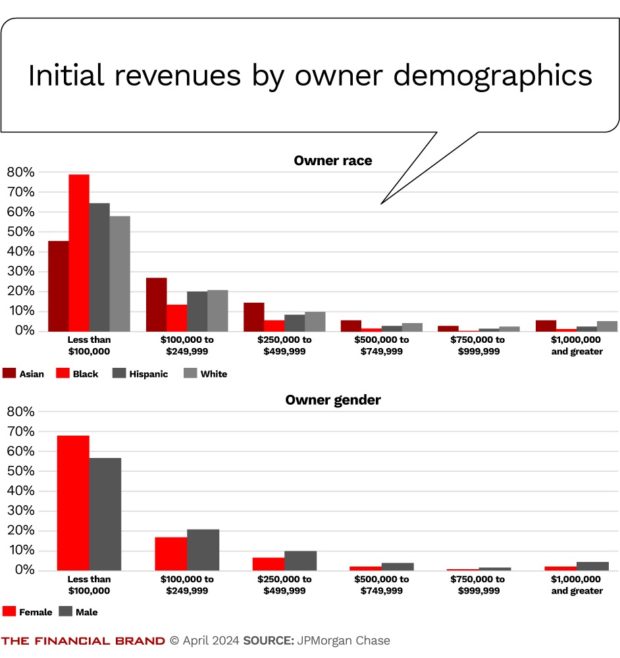

Differences by race and gender: Asian and white-owned businesses had a higher incidence of reaching $1 million within five years of starting the company compared to Hispanic and Black-owned firms. Additionally, a larger share of Asian, white and male-owned firms reached $1 million for the first time in each of the first five years compared to Black, Hispanic and woman-owned firms.

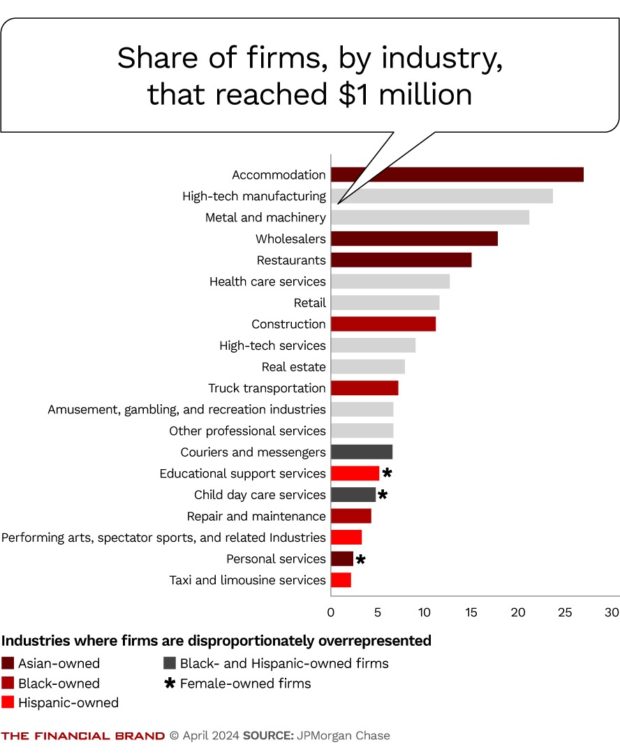

Industry: JPMorgan Chase explored whether the industry could influence disparities as it, in part, directs the nature of revenues and owners of certain races and genres tend to start businesses in specific industries. However, researchers then probed deeper, conducting a regression analysis that accounted for industry, owner race and gender. It showed that companies owned by underrepresented groups in most industries demonstrated slower growth.

Read more:

- The SMB Pain Points That Spell Opportunity for Banks

- A ‘Pivotal’ Moment: What’s Next for Commercial Banking?

- Learn more about business banking strategies.

How Banks Can Help Small Businesses

JPMorgan Chase notes that banks and financial institutions can play a vital role in helping reduce racial and gender disparities related to small business growth and opportunity.

Startup and growth capital: The study found the incidence of scaling to $1 million in revenues was the lowest among firms with the lowest revenues in their first year. This suggests disparities in startup capital and other resources in the initial year. While banks and other financial institutions may not be positioned to meet all small business financing needs, innovative efforts to service female business owners and business owners of color could help these businesses get a stronger start.

Demand side: The report notes several factors that could impact whether and to what extent a small business owner uses financing from financial institutions. First, small business owners must be aware of financial products, understand the application process, be willing to complete it and accept the financing terms.

Chase notes the industry can grow demand by making information about financial products more available to small business owners. Banks can also promote a more straightforward and seamless application process and strengthen relationships with other banks and financial institutions.

Supply side: On the supply side, banks must offer financing products that address the business owner’s needs. Products must be made accessible to potential borrowers and financial institutions must ultimately decide when the owner applies. Banks can also increase the supply of financing by creating more products that serve the diverse needs of customers. Finally, they can expand the credit box by using alternative underwriting criteria or by offering credit score development for those small businesses with low credit scores or thin financial histories.

Disparities in personal savings: Business owners often cite personal savings as the most common source of startup financing. However, there are notable disparities in how much startup capital is available to those when viewed by race and gender. For example, Asian and white owners’ firms are likelier to use larger amounts of startup capital than Black and Hispanic-owned firms.

As of 2019, the median household wealth of Black households ($14,100) and Hispanic households ($31,700) was notably lower than the median network of non-Hispanic white ($187,300) and Asian households ($206,400). Chase notes that policies and interventions aimed at building wealth and savings for Black and Hispanic households may help these business owners gain more access to capital at startup, potentially putting them on a more robust growth trajectory.