Seed Capital Investors Focused on Fewer, Bigger Deals in 3Q

As expected, third-quarter seed funding dropped sharply in the third quarter in New York’s Silicon Alley.

As expected, third-quarter seed funding dropped sharply in the third quarter in New York’s Silicon Alley.

Fintechs were hit particularly hard, but let’s set that aside a moment. The numbers raise an interesting question: Is the venture community trying to cure the indigestion it got by swallowing too many new companies like a python consuming an antelope?

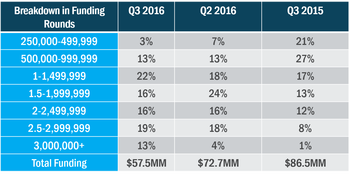

Deals raising between $250,000 and $3.5 million slumped 29% from 2Q 2016 and tumbled 57% from the year earlier period to 32, according to Primary Venture Partners. But the dollar amount raised, though it declined, wasn’t hit as hard — $57.5 million, down 34% from a year earlier and 21% from the second quarter of 2016.

Dig a little deeper and you’ll discover that VCs were doling out larger sums to the lucky term sheet winners: In 3Q 2016 only 1% received more than $3 million; in 2Q 2016, that nudged up to 4%. Last quarter? 13% snagged $3 million-plus investments. In the most recent quarter, 86% of investments were $1 million or more, up from 51% the previous year, and 80% in the 2Q 2016.

This development put me in mind of a widely-read blog post by First Round partner Josh Kopelman on the boom in seed funding in the first half of the decade. That was back in the spring of 2015 when seed funders had poured $4 billion into early stage companies. It was so easy to raise money back then that most deals were substantially oversubscribed. But only the seed round expanded — the amount of dollars available to these young companies didn’t increase further down the road.

Kopelman estimates seed money outpaced Series A by 4:1. The results were ridiculously predictable: the precipitous dropoff/death of early stage winners. The Series A Crunch is now biting back. Kopelman offered sound advice in his 2015 post, and the Primary Venture numbers hint that early stage investors are paying attention:

When you raise seed money, you’re raising on the strength of your vision. As I always say, there’s nothing like numbers to fuck up a good story. And that’s exactly what happens at the Series A.

You’re suddenly judged on the data that you should have been collecting all along to show traction, growth, potential. So why not raise $2.5M in seed money instead of $1.5M to give yourself the best shot at perfecting this data? You should target 18 to 24 months of runway post Series Seed. The best time to raise follow-on capital is when you don’t need it, and 2 years of runway gives you the best chance to land in that situation.

A word about fintech seed raising in 3Q 2016: Only one raised money — Offrbox, with $500,000. In Q2 there were five fintech seed deals, 11% of the flow. Here’s the shorthand for the current fintech seed crunch –the blowups at Lending Club and OnDeck, whose IPO has tumbled 80% from its launch in December 2014.

But fintechs are showing long-term strength in the New York region. Primary Venture writes:

A recent report by Accenture and the Partnership Fund for New York City noted that for the first three months of 2016, New York received more FinTech venture financing than Silicon Valley – $690 million in NYC compared to $511 million – reaffirming the city’s rise as a FinTech hub.

Let’s hope these New York fintech startups can survive and prosper and live to see Series A.