Today’s Bank Secrecy Act (BSA)/anti-money laundering (AML) and fraud departments are busier than ever. On top of managing ever-changing regulations and more complex financial crime schemes, COVID-19 has created even more obstacles for BSA/AML and fraud departments to juggle. To benchmark the industry’s challenges and key areas of focus, Abrigo polled more than 300 BSA/AML and fraud professionals in its inaugural 2021 FinCrime Industry.

Top Challenges and Hot Topics: Key Considerations for Today’s BSA/AML Professionals

August 4, 2021

Read Time: 0 min

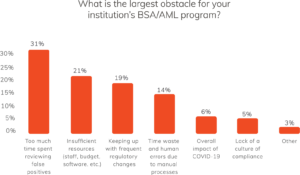

Managing the volume of alerts is a common challenge for BSA officers – especially when many of those alerts are false positives. Nearly one in three respondents said their BSA/AML program spends too much time reviewing false positives, making it the top obstacle for financial institutions for those surveyed.

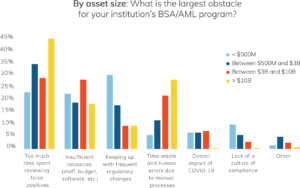

While this was the most commonly reported obstacle overall, a deeper dive into the data reveals that financial institutions under $500 million are particularly hamstrung by changing regulations – the top obstacle reported for this asset size. A key reason for these obstacles may be attributed to the lack of resources financial institutions have access to – the second most common obstacle reported – including staff, a sufficient budget, and software.

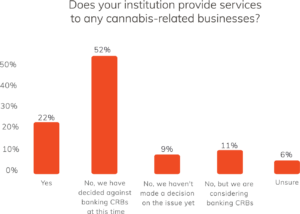

Although cannabis is now legal – either medically or recreationally – in most states today, it remains illegal on a federal level, hamstringing cannabis-related businesses (CRBs) from accessing traditional financial accounts. As this industry continues its rapid expansion, it is increasingly important that it has access to traditional banking services. However, there are not many financial institutions willing to take the risk at this time. Just 22% of financial institutions said that they are currently banking CRBs. However, 11% of those surveyed reported that their financial institution is still considering banking CRBs. These institutions could help satisfy the increase in demand for these services. Understandably, there are still many financial institutions that are skeptical of the risk. Nearly three-quarters of respondents are not currently banking CRBs. While some financial institutions are still weighing the decision, half of the respondents reported that their financial institutions have decided against banking CRBs.

Perhaps even more vexing than banking CRBs is understanding how to handle cryptocurrency. Currently, there are no federal guidelines on banking cryptocurrencies, and it is up to each institution to set policies and procedures for banking cryptocurrencies. Only a third of respondents said that their financial institution had tailored customer due diligence questions or other KYC/KYT measures in place to identify cryptocurrency customers, and only 8% are currently handling any cryptocurrency- or virtual currency-related businesses.

About the Author