Financial crime is a pervasive threat to banks, credit unions, FinTechs and other financial institutions (FIs) the world over. A recent study from PwC found that 47 percent of companies had experienced fraud at least once in the past two years, with a grand total of $42 billion in funds stolen over this period of time.

Financial crime is a pervasive threat to banks, credit unions, FinTechs and other financial institutions (FIs) the world over. A recent study from PwC found that 47 percent of companies had experienced fraud at least once in the past two years, with a grand total of $42 billion in funds stolen over this period of time.

One of the most common threats to FIs is identity fraud, with fraudsters posing as consumers to gain access to their accounts or apply for loans they have no intention of paying back. Other fraudsters leverage more sophisticated techniques like synthetic identity fraud, in which they cobble together wholly fictitious identities with which to conduct their schemes.

The September Preventing Financial Crimes Playbook explores the latest financial crime developments, including the growing threat of identity fraud, the onboarding and artificial intelligence (AI) systems used to curb it and how the COVID-19 pandemic is effecting fraud techniques as well as financial crime prevention efforts.

Developments Around The Financial Crimes Space

Developments Around The Financial Crimes Space

Senior citizens are the demographic group most vulnerable to identity fraud, as they are often not as digitally savvy as their younger counterparts nor as adept in online security best practices. A study from the Cifas National Fraud Database found that identity theft against consumers over the age of 61 rose by 22 percent in 2019, contributing to an 18 percent increase in identity theft overall. There were 223,163 cases of identity theft that year across all generations, with 42 percent of them consisting of bank and credit card fraud.

The ongoing COVID-19 pandemic has only made the threat of identity fraud worse, as fraudsters work to exploit the economic insecurity gripping much of the world. The Financial Crimes Enforcement Network (FinCEN) recently issued a warning that malware, phishing schemes, extortion and business email compromise are in fact all on the rise. Some fraudsters are even impersonating government officials and asking for personal information for stimulus payments, for example, while others are targeting cryptocurrencies.

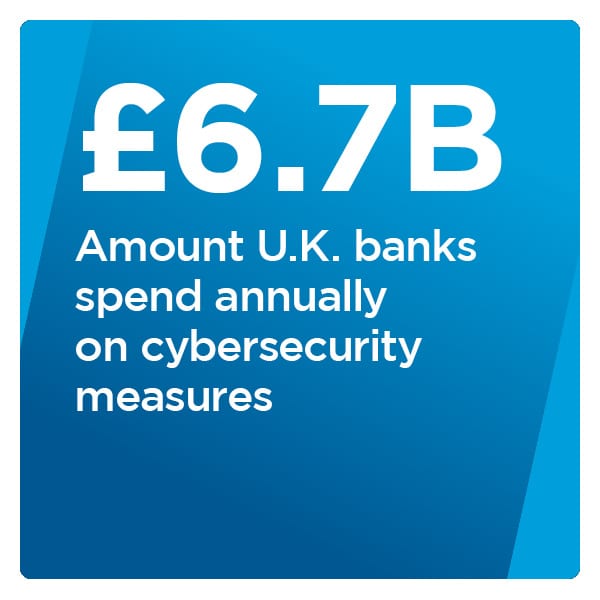

Large investments in security measures are necessary for banks to protect themselves and their customers from this menace. British banks spend upward of £6.7 billion ($8 .9 billion) annually on cybercrime prevention efforts, according to a recent study, with many of these investments devoted to cloud-based systems that harness data analytics. These systems are also designed to ensure compliance with government regulations for fighting organized crime rings, with Thomson Reuters reporting there were 80,000 regulatory updates around the world in 2019 that banks must comply with or be punished with fines.

.9 billion) annually on cybercrime prevention efforts, according to a recent study, with many of these investments devoted to cloud-based systems that harness data analytics. These systems are also designed to ensure compliance with government regulations for fighting organized crime rings, with Thomson Reuters reporting there were 80,000 regulatory updates around the world in 2019 that banks must comply with or be punished with fines.

For more on these and other financial crime news items, download this month’s Playbook.

Fighting The Rise Of Corporate Banking Fraud With AI And Machine Learning

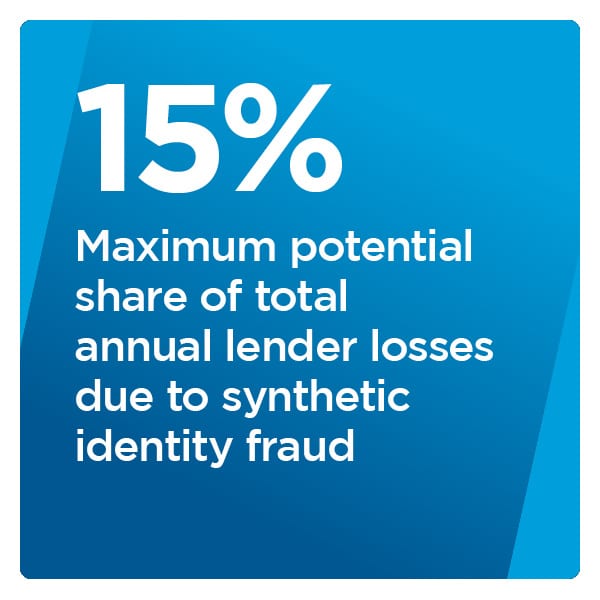

Identity fraud is a pervasive threat, with fraudsters stealing identities and constructing fake ones to make off with $16.9 billion in 2019. Technologies like video onboarding and AI have shown promise in facing this threat, but each is vulnerable when deployed alone. In this month’s Feature Story, PYMNTS talked with Sameer Shetty, head of digital banking at the Mumbai-based Axis Bank, about how these two technologies combined form a multilayered fraud defense system that can make identity fraud nearly nonexistent.

Deep Dive: How Banks Are Threatened With Identity Fraud

Deep Dive: How Banks Are Threatened With Identity Fraud

Fraudsters leverage identity theft toward a variety of ends, including stealing the personal information of bank customers or taking out loans using their names. Some fraudsters deploy synthetic identities rather than stealing them for their schemes, but the end result is equally as damaging. This month’s Deep Dive explores how various identity fraud methods target banks and their customers, and how technologies like artificial intelligence and biometrics are being deployed to counter them.

About The Playbook

The monthly Preventing Financial Crimes Playbook, a NICE Actimize collaboration, offers coverage of the most recent news and trends the financial crime prevention space.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More