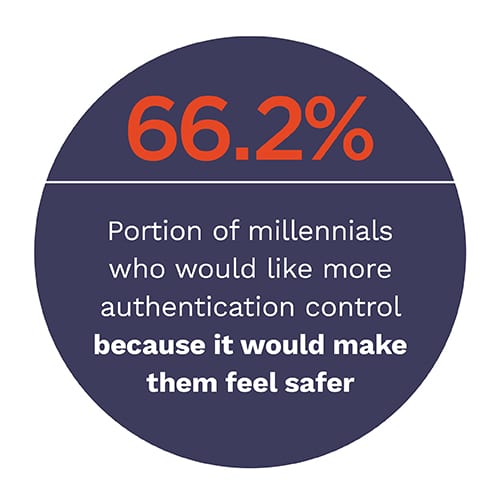

Though many banks may be betting big on advanced technology to help them in the fight against financial fraud, their customers would feel more secure if they were given more control over their banking apps’ authentication processes.

Though many banks may be betting big on advanced technology to help them in the fight against financial fraud, their customers would feel more secure if they were given more control over their banking apps’ authentication processes.

There is a simple explanation for this: Recent PYMNTS research has shown that most consumers believe they are in the best position to tell when someone else is using their accounts, and that they would be better than banks at identifying the presence of fraudsters on their banking apps. Specifically, 72.1 percent said their apps’ security would be stronger if they — rather than their banks — had more control over the authentication requirements. Providing users with the control they want could, therefore, go a long way to deliver on the safe and secure experience they want.

There is a simple explanation for this: Recent PYMNTS research has shown that most consumers believe they are in the best position to tell when someone else is using their accounts, and that they would be better than banks at identifying the presence of fraudsters on their banking apps. Specifically, 72.1 percent said their apps’ security would be stronger if they — rather than their banks — had more control over the authentication requirements. Providing users with the control they want could, therefore, go a long way to deliver on the safe and secure experience they want.

Yet, the benefits of adding authentication controls go well beyond providing a hypothetical feeling of safety. It could also have a very real, profound effect on how consumers use their banking apps.

For the Consumer-Centric Authentication Playbook: Taking (Authentication) Control edition, in collaboration with Entersekt, PYMNTS surveyed 2,835 U.S. banking customers to find out whether consumers would use their banking apps differently if they had the authentication controls they wanted, and how their usage would change if they did. PYMNTS asked respondents about how much control they already have over their banking apps, if they want more control, if having that control would change the way they use their apps and, if so, how?

The research found that most consumers would not only be more likely to use their banking apps if they had more authentication control, but would likely transact more often. In fact, 42.4 percent of survey respondents said they would be more likely to use their banking apps in general if they had more control over their apps’ authentication requirements, while 54.1 percent would transact via app either “somewhat” or “much” more often.

Even more interesting is how consumers’ propensity to change their app usage varies, depending on how often they use their apps and how much control they already have. Consumers who use their apps at least once per week, and already have a great deal of control, would most likely transact more often if they were given even more control, with 61.4 percent saying so. This compares to 57.4 percent of those who use their apps more than once per week with the same level of control, and just 47 percent of those who use their apps less than once per week with little control over  their apps’ authentication requirements.

their apps’ authentication requirements.

However, current app control and usage only account for two among a wide assortment of factors that can impact how consumers’ app usage could change if they were given more control. The Playbook provides an analysis of how each of these factors impact consumers’ propensity to change how they interact with their banking apps.

To learn more about the concrete ways in which providing banking app users with more authentication controls can boost consumer engagement, download the report.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More