Each morning, 80 percent of American consumers check their phones before they brush their teeth — but they rarely do so for the same reasons. Some pick up their mobiles phones to check Instagram or Facebook, while others open an app to check the weather or the headlines from their preferred news outlets. They spend their days going in and out of a collection of different apps, from calendar apps to weather apps and, perhaps most importantly, their order-ahead coffees apps. But there isn’t one, universal mobile app that consumers can rely on to help them do it all.

Yet, our research suggests that there could be — at least in theory. In June 2019, PYMNTS surveyed 1,037 American consumers to learn about how they used their mobile apps, as well as their interest in using specialized “super apps” designed to help them move seamlessly from one app to the next. When conducting our research, we made clear to respondents that these so-called everyday apps would not necessarily be designed to perform all these functions, themselves, although they could, such as WeChat Pay does. They would simply be more of an interface to the apps that they already built to allow consumers to make access to them easier and more convenient. Would such an app appeal to them?

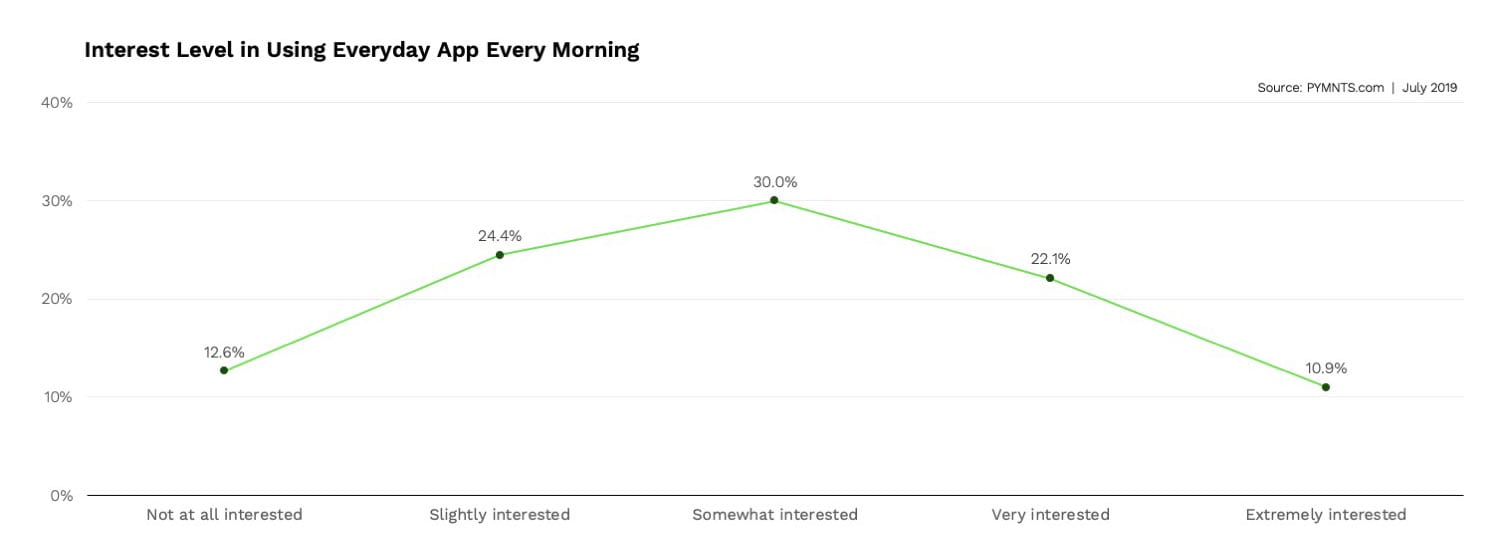

For a third of consumers, the answer is a strong yes, with only 12.6 percent of consumers seemingly vehemently opposed. That makes most — roughly 54 percent — open to the idea, provided they see the value.

Among surveyed consumers, 10.9 percent said they were “extremely interested” in using a hypothetical “everyday app” every morning, and 22.1 percent said they were “very interested.” This appears to signal a strong consumer interest in the idea.

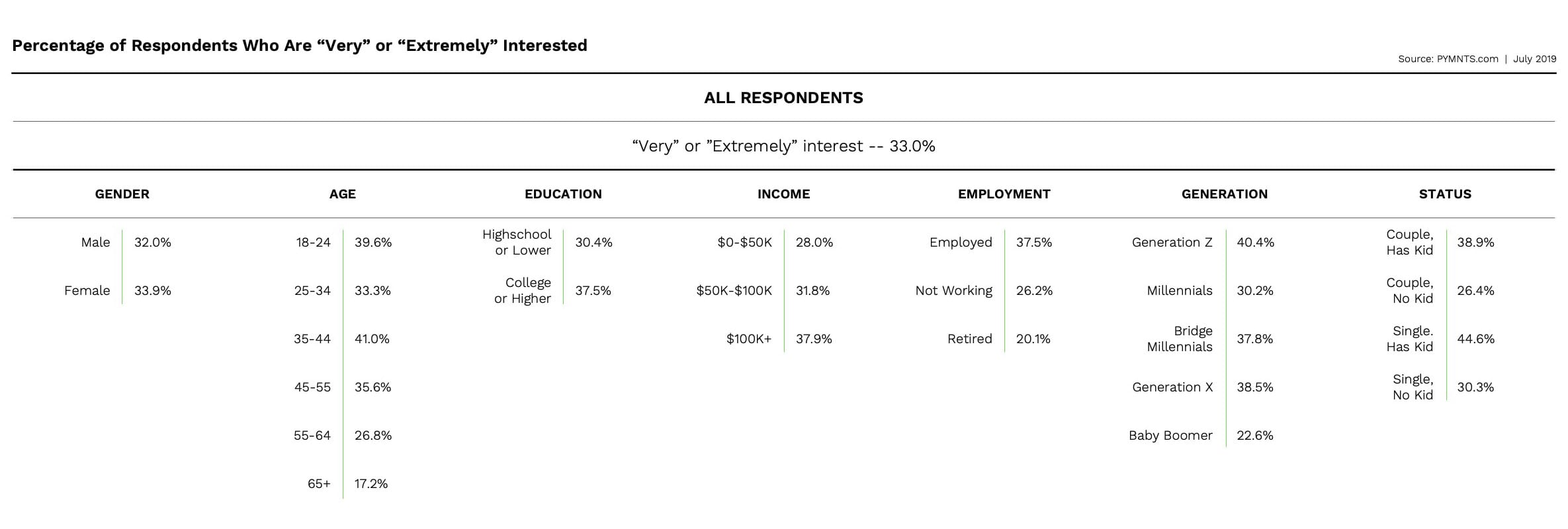

Nor is interest in everyday apps exclusive to any particular age group. Generation Z is most enthusiastic about the idea of using one app for everything, but not by much. In fact, 38.5 percent of respondents from Generation X say they would be very or extremely interested in using such an app, compared to 40.4 percent of consumers in Generation Z. These two groups were the second- and first-most likely age groups to express interest in using everyday apps, respectively.

Then, there are Bridge Millennials. Bridge Millennials are a unique group of consumers, comprised of individuals between 30 and 40 years of age who exhibit cultural characteristics of both Generation X and Millennials. Having had the time to establish their careers, they enjoy higher spending power than younger Millennials, who are just now dipping their toes into the professional world. Among the Bridge Millennials in our study, 37.8 percent said they would be interested in using everyday apps if they were available. The demand for a grand, unifying app is there — just not the supply.

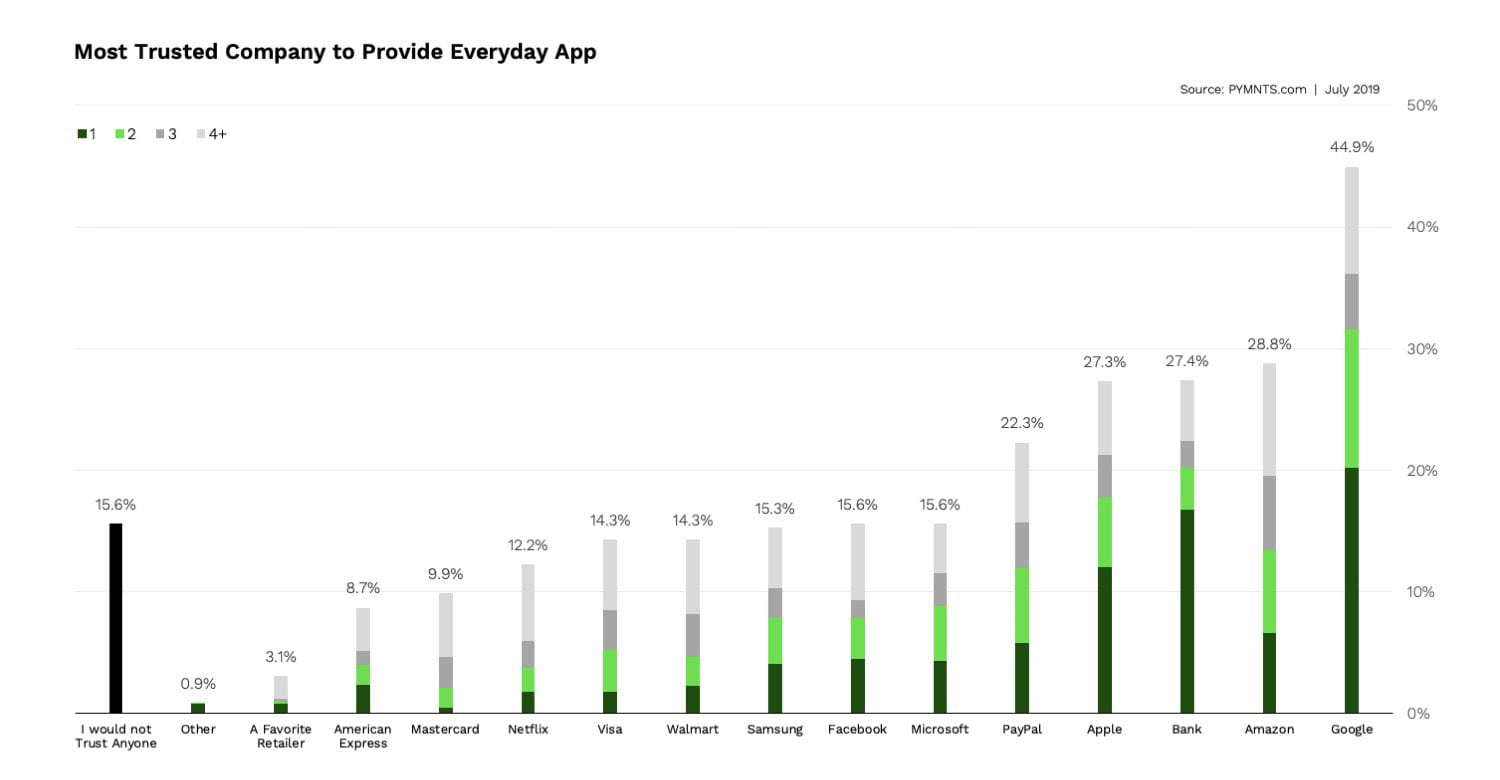

Consumers’ digital experiences are often not as fragmented as their app usage, however. They may keep different apps on their mobiles, but many rely on the same, big tech companies to shop, pay and search the web. Google, Amazon, Apple, PayPal and Facebook are just a few examples of tech companies who are all but omnipresent, and with whom an enormous share of consumers interact with on a daily basis.

It therefore comes as little surprise that these are the same companies whom consumers say they would trust to design, implement and manage hypothetical everyday apps. For instance, 44.9 percent of respondents say they would trust Google, 28.8 say they would trust Amazon and 27.3 percent say they would trust Apple.

Considering how often consumers use these companies’ services, it may not seem like too much a stretch to suggest they extend those services to help streamline their life in other areas. Some consumers use Facebook all day, every data. Others log into their Google or Office accounts to check their emails and calendars. It is easy to imagine how consumers might want to take these digital rituals one step further by attaching that first app to all the others they expect to use throughout their days.

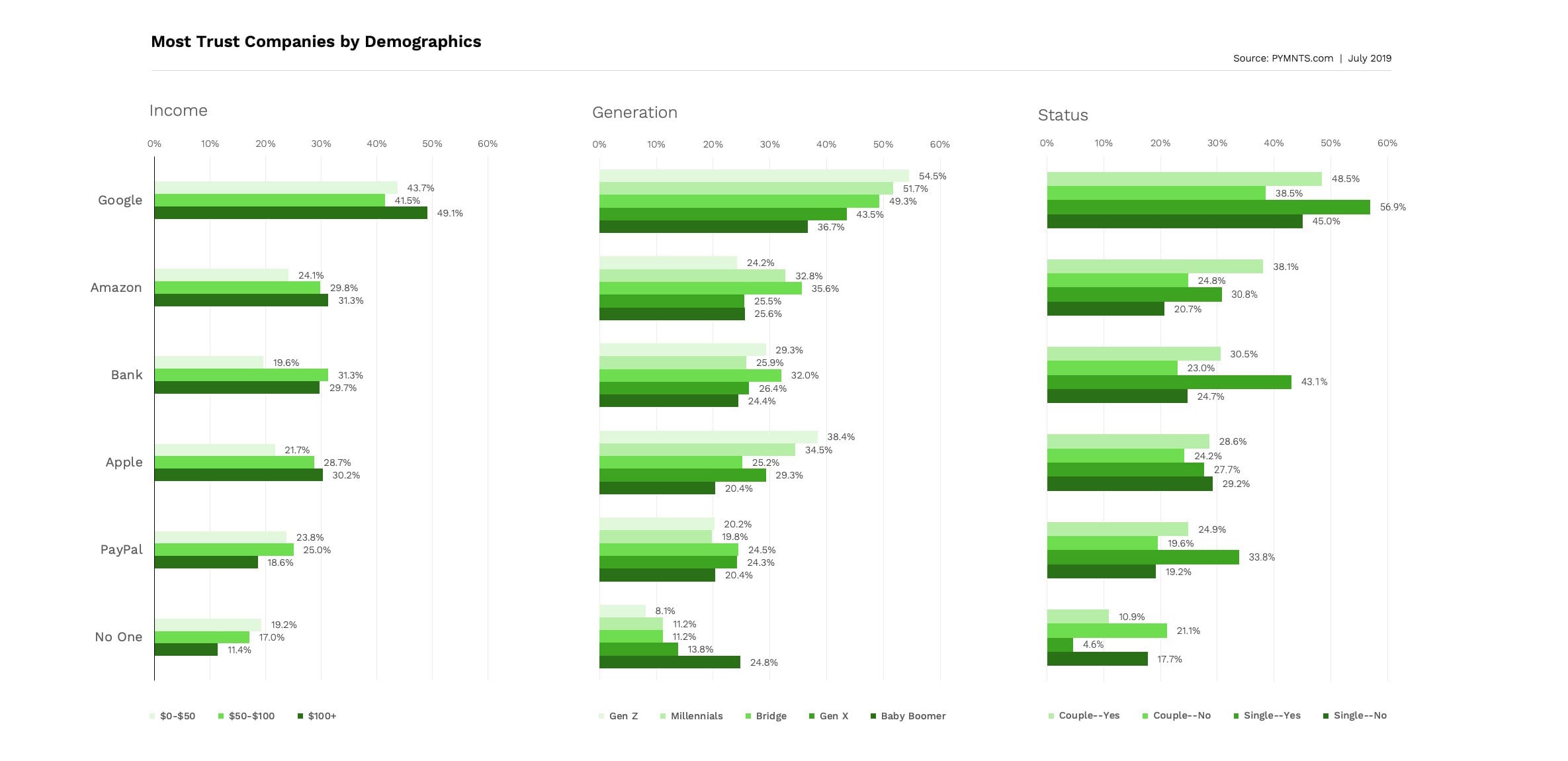

Consumers’ trust in these companies as potential everyday app arbiters varies considerably depending on their demographic profiles, however. Those who earn more than $100,000 in annual income are the most likely to trust companies like Google, Amazon and Apple to support their everyday apps.

On the flip side, consumers earning between $50,000 and $100,000 per year are more likely to trust companies they use to manage their finances and payments like PayPal. Meanwhile, consumers who earn less than $50,000 are the most likely to say they trust no one – at least, not with their everyday apps.

Consumers from different generations also tend to trust different companies. Generation Z and Millennial consumers put more trust in Google and Apple, for instance. Bridge Millennials also express a great degree of trust in these companies, but they are also the most likely to trust Amazon, their banks and PayPal to operate hypothetical everyday apps.

On the flip side of the spectrum are Baby Boomers, who are almost always the least likely generation to trust any company in this capacity.

We also notice a surprising diversity in the levels of trust consumers’ with different relationship statuses place in different companies. When asked which companies they might trust to operate everyday apps, single consumers are the most likely to cite Google, their banks or PayPal, for instance, and couples are the most likely to cite Amazon. Precisely why relationship statuses might affect consumers’ relationships with different companies’ mobile apps is unclear and may require further research to make sense of.

Consumers are also split on whether everyday apps should come equipped with voice-recognition capabilities. Roughly a third (33.7 percent) say they would like everyday apps to include voice features to make them easier to interact with and 21.4 percent say they would prefer to use everyday apps without voice features. But here’s the interesting twist.

Another 10.6 percent of consumers want their everyday app to be their voice assistant, particularly connected to the voice activated devices they have in their homes. In other words, they seem to express more interest in using voice-recognition technology as a means of managing and using the apps they already have — as opposed to clicking and dragging icons on their smartphones.

This suggests that those 33.7 percent of consumers who want to use everyday apps with voice-recognition capability and the 10.6 percent who want those apps embedded into their voice assistants actually desire a very similar, if not identical user experience: This 44.3 percent of consumers want to manage their apps with their voices, creating tremendous room for market growth for voice-recognition-based user interface.

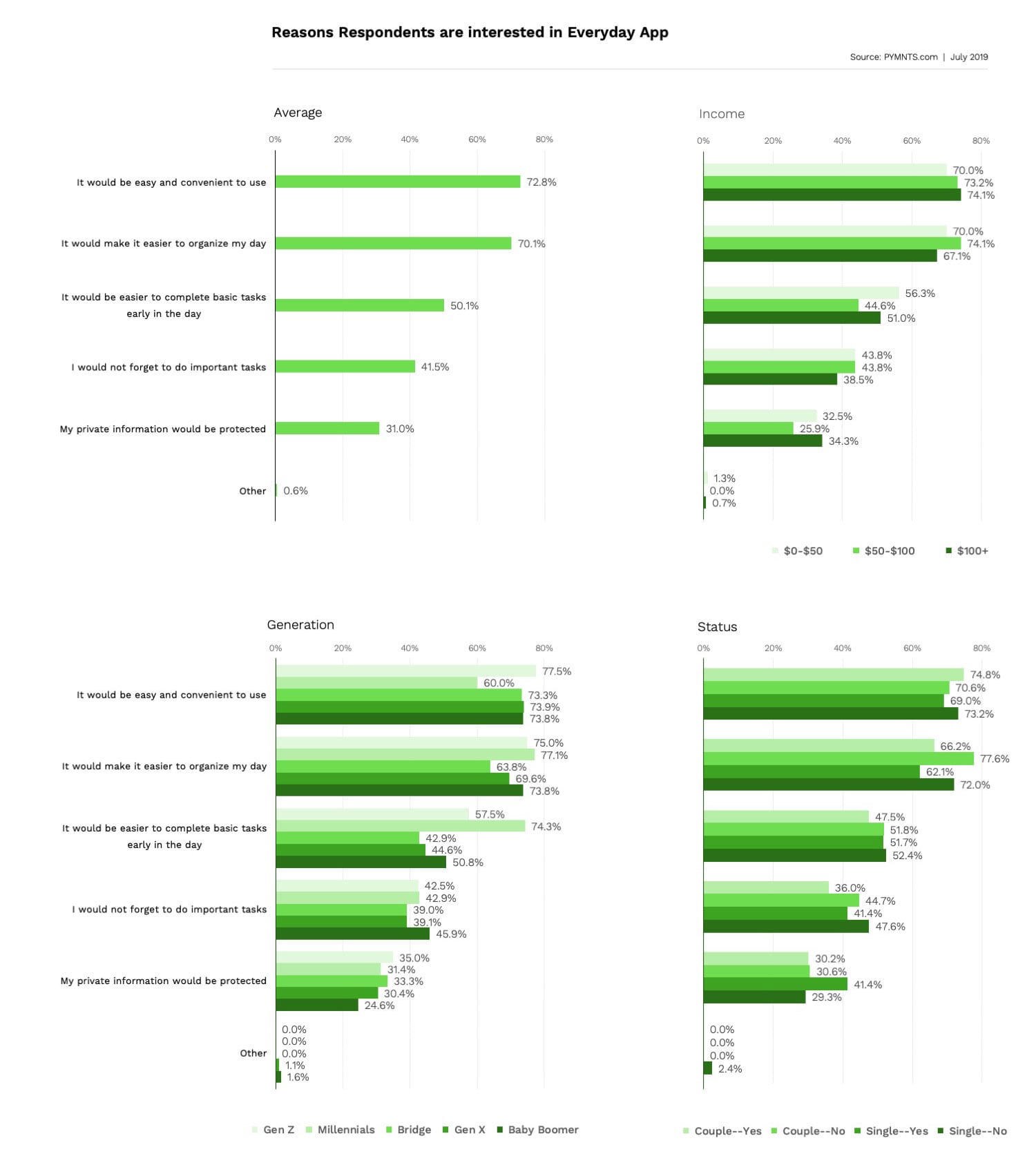

The question of how to achieve it aside, many consumers feel that centralizing the control over these desperate functions in one, conveniently-located “command center” can yield many benefits. Among respondents who said they would be interested in using everyday apps, 72.8 percent said they would be interested because having them would be easy and convenient to use, and 70.1 percent said it would make it easier to organize their days. Similarly, 50.1 percent say linking their mobile activities to these everyday apps would make it easier for them to complete their basic tasks early in the day, and 41.5 percent said that with everyday apps, they would not forget to do important tasks.

That said, consumers also express certain misgivings about the idea of relying on a single app for all their online activities, data security being chief among them. Among respondents who were not interested in using everyday apps, 50.9 percent said it was because of concerns over their data security, and 43.1 percent say they do not want all their information centralized in one place.

What’s more, consumers from different income brackets, generations and relationships seem similarly concerned about these particular points. This suggests that consumers’ general anxiety over data security is the single biggest hurdle to wider everyday app adoptions that companies may need to overcome, if they want to provide this service.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More