Impending 5G technology holds a great deal of promise for many industries, especially for financial institutions. A 5G network could markedly improve mobile banking apps’ speed, security and ease of use.

Mobile banking apps have already enjoyed mass adoption, but what are consumers using them for? And, perhaps more importantly, what do they want from digital banking apps that they aren’t currently getting?

This is the premise of PYMNTS’ new report, Consumer-Centric Authentication Study: Transforming the Consumer’s Digital Banking Experience, with a focus on preferences for authentication controls when banking via mobile.

How Consumers Currently Use Mobile Banking Apps

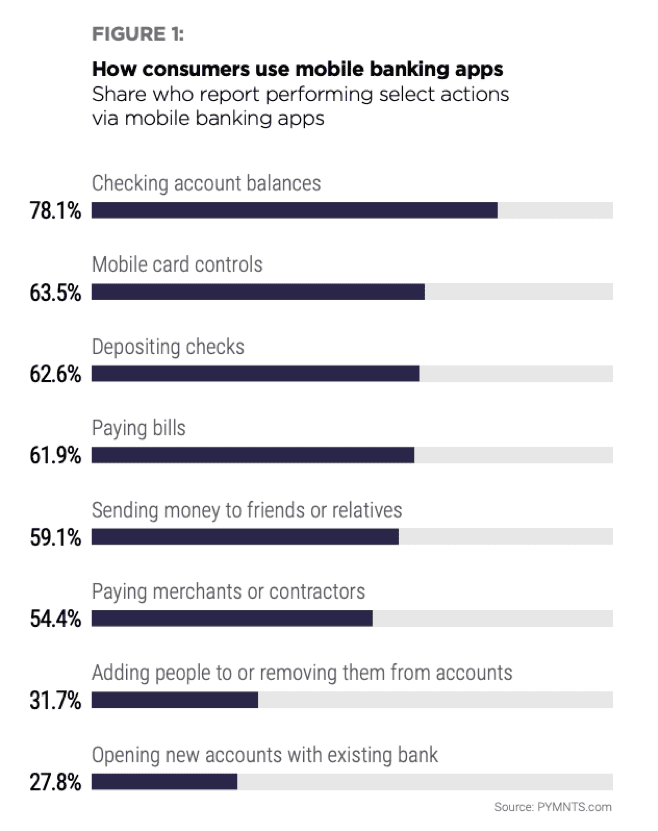

Most consumers (78.1 percent) use mobile banking apps to check account balances. Using mobile card controls (63.5 percent), depositing checks (62.6 percent) and paying bills (61.9 percent) are also popular activities, while sending money to various people is also common. One of the least performed activities is opening a new account.

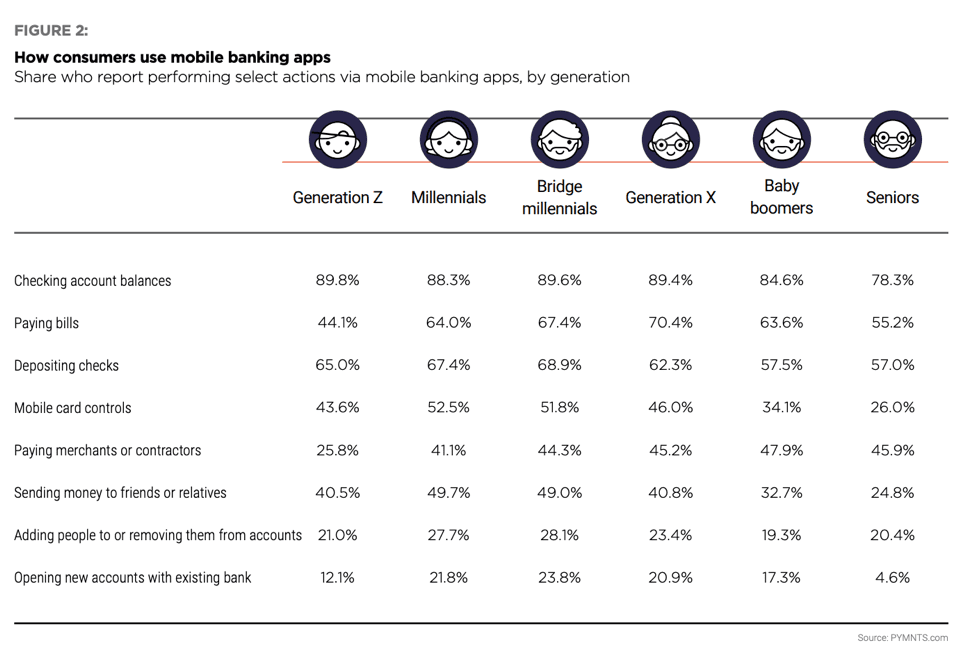

Breaking down mobile banking app activity by generation reveals distinct differences. Just 44.1 percent of Generation Z and 55.2 percent of seniors pay bills via mobile app, while Generation X consumers and bridge millennials are on the opposite side of the spectrum. Bridge millennials were the most likely to use an app to open a new account with a bank (23.8 percent) or to deposit checks (68.9 percent). Generation Z was much more likely to use a mobile app to send money to family and friends than to pay a merchant or contractor.

Consumers Also Want Control

Consumers are given a choice for myriad banking services, but they aren’t given much say in how those services are authenticated. When logging in, 41.2 percent of app users say they must “always” use the authentication methods required by their apps, while 53.2 percent of consumers say they are allowed to choose how they authenticate. Consumers are given even less control over in-app transaction authentication.

Control aside, over one-quarter (25.9 percent) say their mobile banking apps do not require them to authenticate their in-app transactions at all.

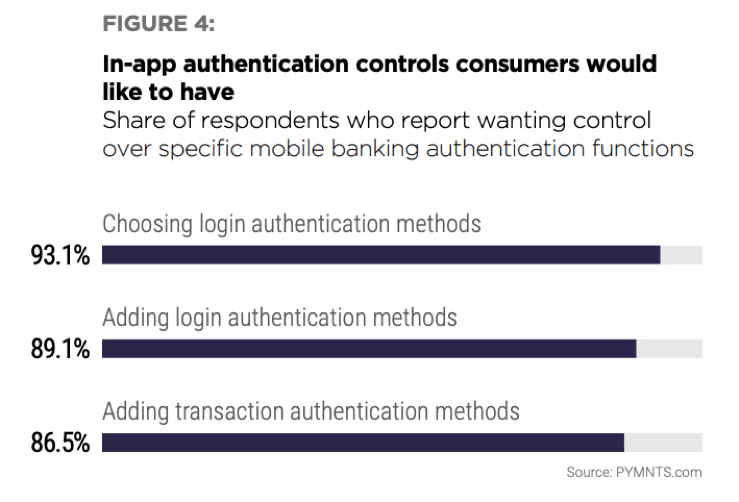

Banks might be underestimating the level of control consumers want over app authentication. Nearly all (93.1 percent) of consumers want to be able to choose login authentication methods, and 86.5 percent say they want to be able to set authentication requirements for different types of transactions made using their mobile banking apps. Though, as mentioned above, only 39.9 percent can actually do this.

A majority (65.5 percent) would like to be able to set authentication requirements for transferring money to friends and relatives, while 25 percent would like to introduce additional authentication requirements for money transfers to friends or relatives. This pattern was consistent for many transaction types. A majority want to be able to authenticate various transactions, and roughly 20 percent to 25 percent would like to be able to choose different methods.

Improving the customer experience is one thing, but the majority of consumers say that having more control over their mobile banking authentication systems would entice them to make more mobile banking transactions – 54.1 percent of consumers say they would transact via mobile either “somewhat more” or “much more” often if they had more control. More control is especially enticing to bridge millennials, millennials and Generation Z consumers.

Much of this desire for control stems from concerns about data security. Nearly three-fourths (71.2 percent) say the security of transactions made via mobile app would be at least “somewhat” stronger if they had greater control over in-app authentication processes.

Beyond feeling safer, 43.1 percent cite improved ease of use and 32.9 percent cite enhanced convenience. Just over one-quarter (26.3 percent) think that greater control over in-app authentication would save time.

The Liability Conundrum

Greater responsibility often comes with greater control.

Many financial institutions do not explicitly state which party is legally responsible for fraudulent transactions that occur via mobile banking apps. Consumers are unclear about whether having more control over in-app transaction authentication would mean they would legally be held more responsible for fraudulent transactions: 40 percent report believing they would take on “somewhat” or “much” more fraud liability.

This isn’t necessarily true, but based on findings from this study, most would still opt for greater control over authentication.

For example, consumers who feel that having more control over their mobile banking apps’ authentication requirements would legally make them “much more” responsible for fraudulent transactions, 76.7 percent would still want at least “somewhat more” control and 60.2 percent want “much more.”

This strong preference for user control could give banks an opportunity to expand their customer base by providing these types of features.

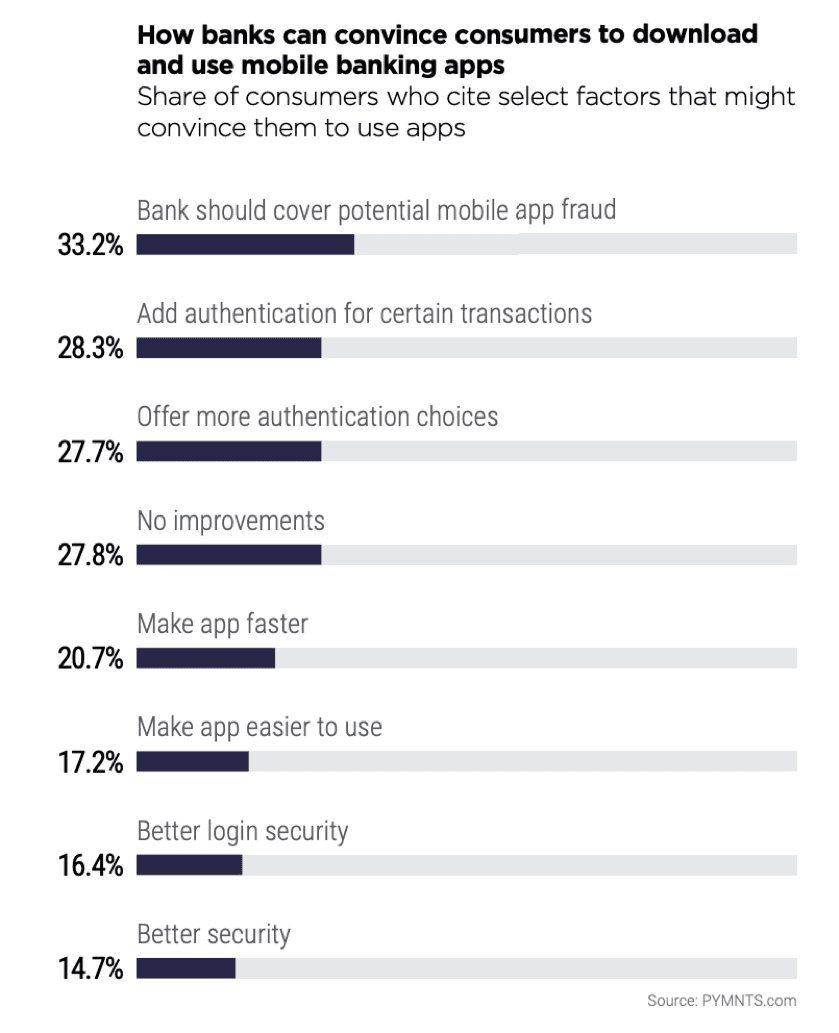

Banks might also benefit from being open with their customers about where mobile banking app fraud liability lies. As eager as many consumers are to obtain more control over their mobile banking authentication methods, 33.2 percent say they would be even more willing to use their banking apps if their banks would clearly communicate which entity covers or is liable for fraudulent transactions.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More