Tax Day for Americans is here, or at least it will be on Tuesday, April 17.

This year is a bit of an unusual year as far as taxes are concerned, since April 15 actually falls on a Sunday. Normal protocol would automatically push the tax filing deadline to April 16, but this year, April 16 marks Emancipation Day in the nation’s capital, and so, as a holiday gift to all of us, the Internal Revenue Service (IRS) has given Americans until April 17 to file their taxes.

Us Bostonians would like to claim partial credit for that two-day extension, since April 16 is Patriot’s Day — a holiday in the state of Massachusetts — and Marathon Monday.

But if those extra two days don’t feel like enough time for those of you who plan to spend the weekend trying to figure out your taxes, there is a bright side.

It’s not 1914.

Granted, there are many reasons to be glad it’s not 1914: penicillin, female suffrage, the polio vaccine, computers, air conditioning, Netflix, the smartphone — all essentials that 1914 didn’t have. What it did have (World War I) no one really wants (or wanted).

But despite the things that 1914 didn’t have, it did have income taxes; the 1040 we all know and love today made its first appearance among the masses that year following the ratification of the 16th Amendment to the Constitution.

Back then, taxes weren’t due on April 15. The 1040 form citizens received in 1914 clearly stated that taxes were due “in the hands of the Collector of Internal Revenue on or before March 1.”

Tax season used to be a month and a half shorter.

Why?

“The long story short is sort of underwhelming,” Joseph Thorndike, a historian with tax publisher Tax Analysts told CNN. “There’s no reason [lawmakers] said March 1 except it’s reasonably close to the end of the prior tax year, but not so close that it’s difficult to get the paperwork ready.”

But, as it turns out, Americans are a nation of procrastinators, according to Thorndike, and it became clear quickly that they needed more time to get their taxes together. The deadline first shifted to March 15, but that didn’t really help; taxpayers still had a hard time with the deadline — as did the IRS.

“Millions of middle class people were paying an income tax,” Thorndike said. “It became clear that there were a lot of people struggling to make the deadline.”

So, the government pushed the deadline to April 15 in 1954 to give consumers a longer runway and the IRS the chance to accommodate a more staggered runway.

That date has stuck ever since, even though it only marginally helped with the procrastination problem.

Americans, as it turns out are …

A Nation of Dedicated Procrastinators

It seems that for a certain — and fairly large — subset of Americans, it really doesn’t matter when Tax Day hits, as those citizens are committed to waiting until the last possible minute regardless.

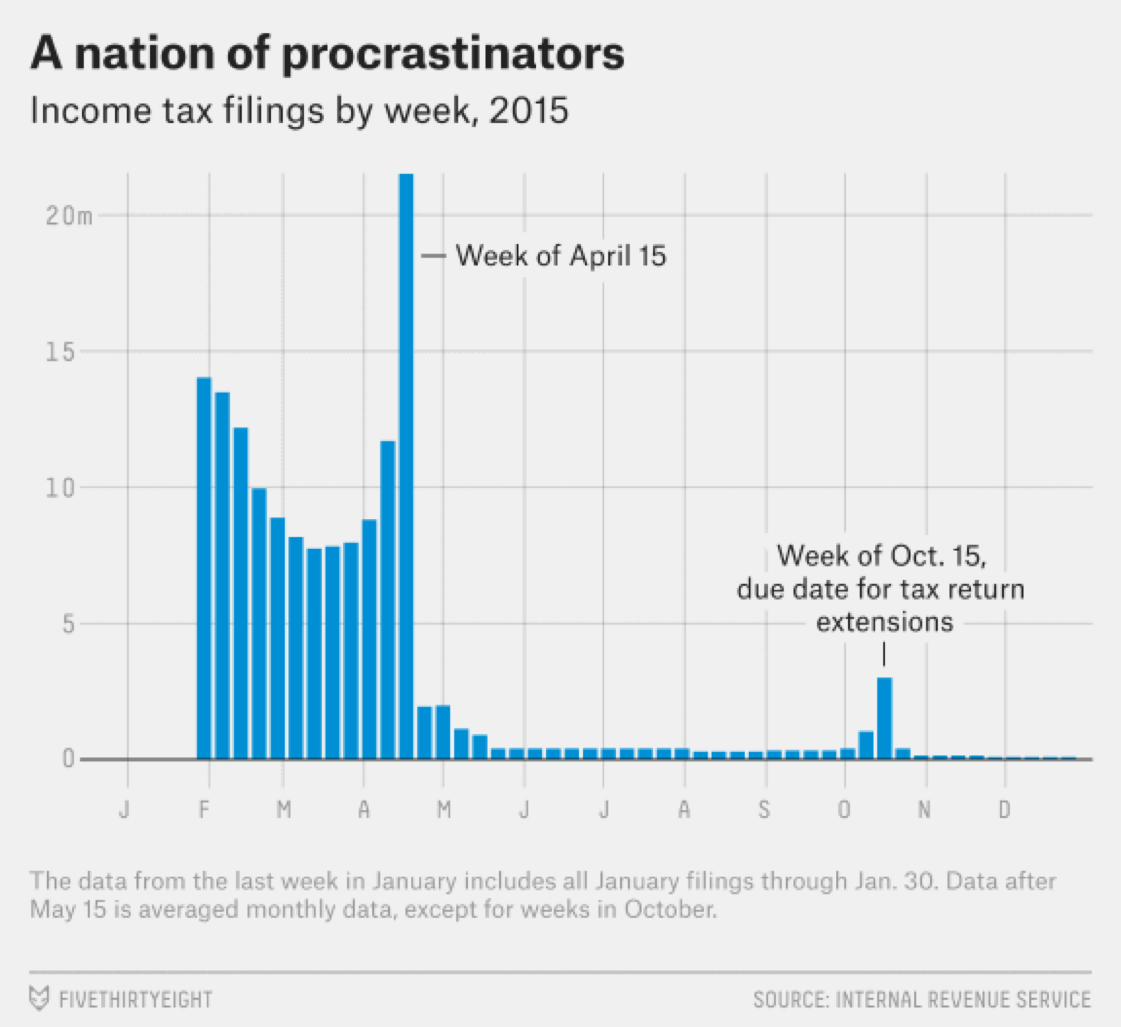

According to FiveThirtyEight, as of three years ago, roughly one in seven citizens consistently wait until the deadline to submit their tax returns and pay their taxes. They also provided a graph to illustrate the not-so-bell-curve look at how Americans pay taxes by calendar date.

There is an initial bump in early February, as early filers expecting a refund get their hands on their W-2s, FiveThirtyEight noted. Those early filers, according to Fiona Greig, director of consumer research at JPMorgan Chase Institute, also tend to be lower income and earmarked for paying bills.

For those expecting to pay taxes, or for those who expect to get a relatively modest refund, the name of the game is delay and right up to the last minute. Unfortunately, it seems to be a growing trend.

Last year, according to Bloomberg, one out of every five Americans waited until the last possible moment to file and pay Uncle Sam.

It’s a trend, Intuit CEO Brad Smith noted, that is unlikely to change because technology and electronic filing have made it incredibly easy to delay until the last second.

“You can just sit in your pajamas or your underwear and use TurboTax,” Smith said in an interview with Bloomberg News. “You just hit send by 11:59 p.m., and you’re good.”

Who wants to pay The Man a minute earlier than they have to?

The Sluggish Bitcoin Filers

Speaking of last minute, among the missing filers are those with bitcoin/crypto profits. Recent data from Credit Karma suggests this sector of Americans have not yet filed their taxes.

According to Credit Karma, of the most recent 250,000 filers, only 100 people (.4 percent) reported capital gains on their cryptocurrency investments.

“There’s a good chance that the perceived complexities of reporting cryptocurrency gains are pushing filers to wait until the very last minute,” Jagjit Chawla, general manager of Credit Karma Tax, said in an emailed statement.

The government, according to Tom Lee — head of research at Fundstrat Global Advisors — should have some pretty significant bitcoin tax revenues rolling in this year, given the growth in the value of those holdings.

Bitcoin saw its value grown 13-fold in 2017, with cryptocurrency markets in general gaining well over $500 billion in paper value. That means U.S. households should owe about $25 billion in capital gains taxes on bitcoin.

Windfall for Uncle Sam?

It’s a question. The IRS views bitcoin as an asset class, subject to capital gains tax when sold. Investors who last year thought bitcoin was going to hit $1 million a coin and didn’t sell obviously owe no taxes.

If an investor cashed out, determining what is owed requires knowing the dollar value of bitcoin at the time of one’s transactions, for which there is now more or less the honor system.

“There isn’t any official reporting mechanism in place,” Sarah-Jane Morin, who is of counsel at Morgan Lewis, told CNBC. “The way the IRS is looking at this: They feel like people should comply and use their best efforts to figure out cost basis.”

Those people better hope their best efforts are correct. The IRS recently warned filers that income stemming from cryptocurrency transactions must be reported on their tax returns. Failing to do so risked them $250,000 in fines and possible prison time.

Still, some experts — like Seattle-based attorney Elizabeth Crouse — suspect that many bitcoin enthusiasts, given who they are and how they feel about taxes, might just take their chances that the IRS is less serious about scrutinizing this than they say they are.

“If I had to guess, there’s probably a lot of underreporting. Most of the people in the cryptocurrency world tend to have a pretty high risk tolerance,” she said.

But others are taking this more seriously. Some analysts have noted that the precipitous bitcoin price slide that has been on display is explicable by a pretax sell-off among crypto investors who are selling to be sure they have the cash on hand to pay the tax man on April 17. As evidence of this theory, analysts said bitcoin’s price has rallied and is up 17 percent over the last two days — indicating that investors have their capital gains taxes in hand and are now ready to begin really trading again.

That remains to be seen. With bitcoin, there is certainty.

But with taxes?

Well, as Ben Franklin once said, “In this world, nothing can be said to be certain, except death and taxes.”

Happy filing!

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More