Paul McCartney and The Beatles may have told us that money can’t buy us love, but new research claims that it can certainly buy us happiness.

And how much money consumers need to be happy.

A recent Gallup World Poll tells us consumers whose households earn between $60,000 and $75,000, on average, have reached the highest level of emotional wellbeing, and more income won’t make them happier.

That means, based on the latest published research of 50,000 households and 135,000 individuals by Sentier Research, many U.S. consumers should be dancing in the streets.

In May, the median household income for Americans stood at $61,858 — the highest since January 2000, after adjusting for inflation. Median household income, which had dropped to $58,829 in June 2011, has consistently increased since the summer of 2014. May 2018’s household income numbers were up nearly 2 percent from last year, they say, due largely to increases in base compensation resulting from a tightening labor market.

Consumers, these data points conclude, should be positively zen-like relative to their household income situation.

Yet, you might not think consumers are so happy if you look under the hood, as we have done.

Are the more than a third of U.S. consumers falling behind on their bills happy?

Or are the 27 percent of the population — those high-income Bridge Millennials and Gen X-ers with college degrees who are steps away from financial catastrophe — happy, even if they do report feeling more positive about the stability of their financial situation than they did this time a year ago?

Those are just two of the findings from our quarterly report on the relationship between credit, credit access and the financial performance of U.S. consumers.

Each quarter, with the support of Unifund, we survey 2,000 consumers who statistically represent the adult population in the U.S. and ask them questions about their current financial situation: their income, the bills they pay, how they pay them, their access to all forms of credit, how they use those forms of credit — questions designed to gauge their financial stability and the steps being taken to improve it. We literally look under the hood of household finances.

We then organize these consumers into personas that reflect their financial and credit performance.

We use statistical methods to analyze their responses. What we found this time, we think, is as insightful and hopeful as it is foreboding.

The Rose-Colored Consumer Credit Glasses

To look at the results across the population at large is to miss the nuances of the financial picture of important swaths of it.

On balance, the U.S. appears to have a population that has its financial act together in the aftermath of 2008’s Great Recession.

And it seems it mostly does.

The average credit score reported of the U.S. consumer is 695, with a third of the population stating that their own score had improved over the last year. Our sample, whose average age is 45, is one in which 60 percent of the population is employed. These consumers earn an average income of $70,000.

Individuals in the $50,000 to $75,000 range report the largest increases in wages over the last year. That sounds pretty good in a market in which wages are stagnating — with base comp rising at 0.5 percent and pay (including bonuses) decreasing by 0.3 percent, despite unemployment levels residing at their lowest levels in 23 years.

Perhaps then, not surprisingly, 83 percent of consumers report that their financial circumstances have improved or stayed the same since last year.

Yet digging deeper exposes some problems.

Despite these seemingly sound, strong financial fundamentals, more than a third of consumers report falling behind on bills, up 6 percent from this time last year, in an economy that is booming with inflation rates below 2 percent for more than eight years.

And that’s not a “Geez, I forgot to pay the credit card bill since I was away for a week” late paying the bills situation.

No, this is different and more concerning — telltale in an era when auto bill pay makes paying bills automatic and being late can reflect a conscious decision to delay or skip a payment entirely.

Those delinquencies also seem to have little to do with income or educational stereotypes: Those with some of the highest incomes and educational levels are among those with the most precarious financial circumstances.

In fact, when you look closely, those most at risk of a financial crisis appear more like those who are totally shut out of the credit markets due to chronic delinquencies than a cursory review of their financial profile might otherwise suggest.

From “No Worries” to Why We All Might Want to Be Worried

The most interesting part of any study like this is finding the stories inside the pile of data that comes back from the field.

It’s what led to the creation of the four personas that we track consistently to gain important insights about the financial performance of the American consumer. Simply looking at age bands or income levels doesn’t do it justice.

We always knew we’d find the extremes — and we did.

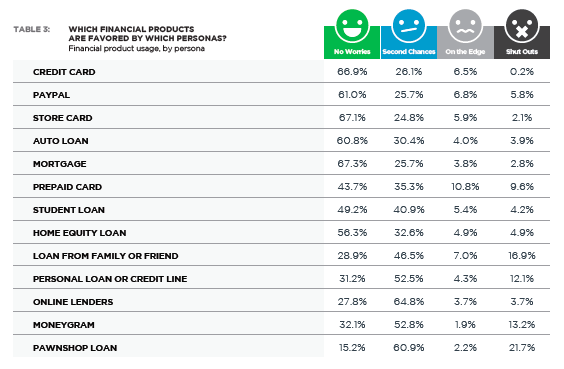

There are the “No Worries” personas — the high-earning, highly educated segment of the population that pays their bills on time; 70 percent report putting money away for a rainy day. They’re about 50 years old and earn, on average, $77,000 a year.

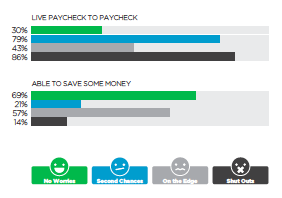

They have access to credit, have mortgages, home equity and car loans. They have and use PayPal accounts to buy things and pay bills. They have and use store cards and say they pay student loans (probably at that age for their millennial kids). Less than a third — 30 percent — report living paycheck to paycheck.

At the other end are the “Shut Outs” — those so chronically delinquent they can’t get the credit they say they need and would like to have. Only 4 percent of Shut Outs report having a credit card.

At 41 years of age, on average, they earn $50,000 a year, and less than half — 47 percent — are employed full-time. Seventy-eight (78) percent of Shut Outs lack a college education and less than 40 percent of them own a home. Since they find themselves shut out of the traditional credit markets, access to credit is predominantly through loans from friends, family members or pawnshops. Not surprisingly, 86 percent of Shut Outs say they live paycheck to paycheck, and only 14 percent say they are able to save money.

Together, these two groups represent about two-thirds of the U.S. population — No Worries at 58 percent, Shut Outs at 7 percent.

Then, we always knew we’d find those who fell somewhere in between.

The “On The Edge” persona appears to be a solid financial citizen: roughly 42 years of age, earning an average of $64,000 a year. More than half, 53 percent, own a home, and 41 percent are college-educated. Seventy-one (71) percent of the On The Edge personas say they are better off financially this year versus last, despite 36 percent reporting working full-time. If we had to guess, we’d say this group consists of gig or freelance workers who don’t work full-time for any one employer, but who do project-based work for many and like it that way. In fact, this is consistent with data from our Gig Economy Index and the percent of U.S. consumers who report doing only gig work.

This group has access to credit but doesn’t use it because they don’t like or want to. Their key to feeling chill about their financial circumstances is that they don’t report having debt payments larger than their monthly income.

Fewer than 7 percent (6.8 percent) say they like and use credit cards regularly. Despite being college-educated, only 5.4 percent report having student loans. Only 43 percent of them say they live paycheck to paycheck, and more than half — 57 percent — say they save money. They were given the mantra “On The Edge” since they straddle the consumer credit market; they can get credit if they wanted to but, for their own reasons, have chosen to opt out.

Then there are the “Second Chances” — the persona group that has had a shock to their financial situation typically through a job loss or divorce. That shock caused them to lose credit, and then, after getting out from under that shock, they’ve been given a “second chance” at reestablishing that credit on the basis of their profession, current income and earnings potential.

The On the Edge and Second Chances represent more than a third of the population — Second Chances at 27 percent and On The Edge at 8 percent.

What we didn’t know, until this last study, was how similar financially the Second Chances are to Shut Outs — for as different as their demographic profiles suggest they are.

And the ticking time bomb that the Second Chances may be for the lenders, merchants and the economy as a whole if they and we don’t do something to intervene.

Meet the Second Chances

By all accounts, Second Chances look like the American Dream.

They are 42 years old and earn $63,000 a year. Sixty (60) percent of them own their own home and are employed full-time. Forty-one (41) percent have college degrees. Sixty-six (66) percent have credit cards. Seventy-seven (77) percent report they are better off or the same, financially, as they were last year.

Yet, 79 percent of them also report living paycheck to paycheck.

Half (50.6 percent) of Second Chances say their monthly bills are larger than their monthly income, with the other half reporting that most of the time bills outweigh their monthly income. It’s not surprising, and perhaps even predictable, that 50 percent also say they will either fall into delinquency (22 percent) or struggle to pay (28 percent) their bills three months or less from now.

That’s an even more pessimistic view than their Shut Out counterparts — only 7 percent of whom expect to face a similar uptick in delinquencies over that same timeframe.

It’s also not surprising that only 21 percent of Second Chances report being able to save any money at all.

Perhaps the better way to state this is that, on the face of the data, it’s remarkable as many as 21 percent can save any money at all — despite an income that is 20 percent more than Shut Outs, 14 percent of whom report an ability to save money, and one that is more or less consistent with their On The Edge counterparts, 43 percent of whom say they are saving money.

What accounts for the difference in self-reported financial stability and the ability to save despite positive employment and income prospects?

What accounts for the difference in self-reported financial stability and the ability to save despite positive employment and income prospects?

Their use of consumer credit products.

While credit cards and store cards were two of the top three financial services products used by our sample (the third was PayPal), Second Chances were far more likely to use personal loans from non-banks, online lenders or loans from family or friends to cover their expenses. This group was far more likely to use pawnshop loans to cover short-term expenses and credit cards to cover the cost of day-to-day living expenses.

The Second Chances group also reported favoring MoneyGram as a way to pay their utility bills. Why? It’s the only way to pay bills the same day, using cash, and avoid having service shut off.

This group also has a heavy student loan debt burden — nearly 41 percent report they owe money to their alma mater.

That college education, though, is one of the reasons this group remains optimistic about their future financial prospects.

Eighty-five (85) percent of Second Chances believe they can earn enough to cover their financial expenses.

Provided, of course, that they find a way to survive while getting there.

And provided, of course, the economy keeps humming.

Meet the Financial Invisibles

The economy sure is humming now.

The Commerce Department reported that May retail sales in the U.S. rose 1.3 percent — the largest increase in retail spending since the fall of 2017. Economists predict that June retail sales will increase by .5 percent over May’s impressive retail spending performance. That’s a big deal, since consumer spending drives more than two-thirds of U.S. GDP.

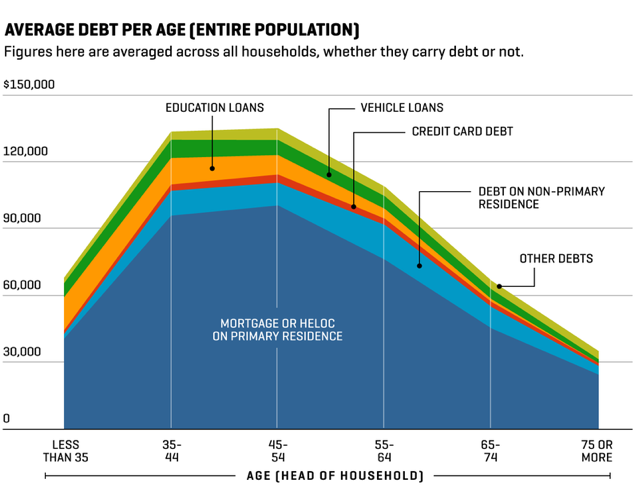

Source: http://time.com/money/5233033/average-debt-every-age/

At the same time, the Federal Reserve quarterly study of consumer debt says consumers are racking it up. Today, U.S. consumers owe roughly 26 percent of their annual income to debt, up from 22 percent in 2010. That amounts to $13.2 trillion, up 18.5 percent since 2012.

Ten (10) percent, the Fed says, of household income is allocated to debt payments for automobiles, credit cards, personal and student loans. Debt service on credit cards has declined, even as credit cards as a percent of debt has been on the rise. Balances on credit card debt declined by 2.3 percent last quarter, as have delinquencies on that debt.

What’s driving up debt and debt service, the Fed reports, are the balances on student debt, mortgage and auto loans which have increased by 2.1 percent, 0.6 percent and 0.7 percent accordingly and will likely rise more as interest rates rise further.

Perhaps recognizing that, these Second Chances say what they need most is more access to credit, since that’s the only way to pay the bills. And once traditional options have been tapped out, they’ll turn to alternative players — maybe some good, maybe some not so good — to make ends meet.

But this group, more than any other, also has a strong interest in financial education to improve their future financial prospects, their credit scores and the ability to gain access to cheaper forms of the credit they feel they need to move beyond the stress of their paycheck-to-paycheck existence. Tools and tips to help them manage their way through their current situation are seen by this group as highly valuable.

Like every other aspect of their lives, they want tools that make it easy and convenient to create certainty in one part of their financial lives that may not be as certain as it might otherwise appear.

There are a number of creative innovators developing schemes trying to do that. Some offer kinder, friendlier versions of short-term, small-dollar credit and consumer-friendly debt consolidation programs.

Some are making it possible for employers to offer earlier access to wages earned and proactive suggestions on how to manage the money they have earned with the bills they need to pay.

Technologies are making it possible for money to be pushed to consumers and used within seconds of it being sent, including for employers who’d like to pay their workers on the weekend.

Card issuers are getting more creative too about the design of their credit products by offering generous cash back on purchases to offset spend, allowing reward points to be turned into money to pay for things, and even offering the option to finance specific larger-ticket purchases separately from payments on monthly balances.

It’s a start.

Perhaps most interesting about these Second Chances is that they don’t look like they’re in trouble. They have good jobs. They wear nice clothes. Their kids probably go to summer camp, and they take family vacations. Walking by them on the street or working in the cube next to them would never foreshadow the stress of their daily financial situation.

They are the Financial Invisibles in search of a solution, although they don’t appear, on the surface, to need much of one at all.

The Second Chances are a big driver of the economy and a bellwether of our future economic prospects.

Some may say they’re living beyond their means, and maybe some of them are. But most may be at the same point in their lives that their parents were at their age — married, kids, house, car and dog.

But without some of the things that their parents had: the certainty of a steady job, pensions, guaranteed raises and bonuses year after year, savings, a house with equity that could be tapped into to pay for big expenses.

Unless we sort this out as a payments financial services ecosystem, we’ll be talking about things a lot more serious than a bunch of consumers feeling stressed out about paying their bills but managing to pay them somehow, some way, even if they’re late in paying them.

Of course, maybe the Financial Invisibles are happy, as Gallup would have us believe, because they’ve reached this bliss point of income. Looking under the hood of their household finances, they look like they should be worried, and if they aren’t now, they easily could become very worried with the next downswing.

Which, as we all know, is inevitable.

And yes, the economy is definitely humming, but most people are still living paycheck to paycheck and facing financial stress.

Money can’t buy love, but at least for now, it helps to take the kids to Disneyland.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More