This post was substantially updated from the one originally published February 28, 2020.

Countdown to CECL: A timeline for credit unions

April 1, 2022

Read Time: 0 min

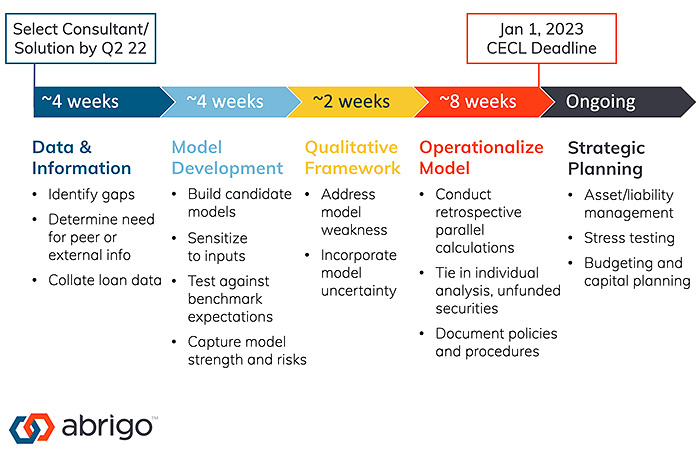

Large SEC filers have officially adopted the current expected credit loss standard, or CECL, for recognizing credit losses, and other financial institutions are eager to learn from their CECL implementation efforts. While credit unions have until 2023 until they must comply with CECL, many institutions were caught up in “analysis paralysis” in their transition, delaying their preparations. Add a global pandemic to the mix, and CECL implementation has been on the back burner for many financial institutions. Experts and 2020 adopters have repeatedly stressed the importance of preparing early. “If you’ve kind of been dragging your feet on this, now is the time,” said Brandon Quinones, Director of Client Education at Abrigo. “The bottom line is, there are no benefits to starting early because it is no longer early. The time is now to ensure you are ready for January 1, 2023.”

If you’re eager to get planning, but struggling to set goals for CECL implementation, review FASB's CECL Prep Kit and consider this timeline:

About the Author